$3.2 billion invested in pps! teda group’s new force aims for world’s largest pps capacity—what enables its challenge to japan’s toray technologies?

On May 6, 2026, in the Rudong Yangkou Port Economic Development Zone of Jiangsu, a signing agreement has drawn significant attention from the plastic industry. The signatory is Jiangsu Dongtai Qixin Technology Co., Ltd. The content of the agreement: a project to produce 160,000 tons of polyphenylene sulfide (PPS) annually, with a planned land area of 150 acres, to be constructed in two phases, and the first phase investment is 1.6 billion yuan.

This is the second time that Dongtai Qixin has taken action in less than 9 months.

Turning the clock back to August 28, 2025, in Huangshan, Anhui, the newly established Dongtai Qixin Technology Co., Ltd. of Huangshan, which had only been founded for 5 months, also boasts an astonishing project scale: a total investment of 1.6 billion yuan, with plans to produce 80,000 tons of PPS annually. The first phase is expected to go into production in June 2026.

With theof the two bases, the total production capacity of Dongtai Qixin has reached 240,000 tons/year - a figure that exceeds the combined annual production capacity of global PPS producers in 2024 (the global PPS production capacity in 2024 is approximately 210,000 tons/year). (Note: The term "" is translated as "" because it directly refers to the action of adding or stacking, and there's no exact single English word that captures its meaning in this context. For better readability, it can be replaced with "combination" or "integration" in the sentence.) Revised for better readability: With the combination of the two bases, the total production capacity of Dongtai Qixin has reached 240,000 tons/year - a figure that exceeds the combined annual production capacity of global PPS producers in 2024 (the global PPS production capacity in 2024 is approximately 210,000 tons/year).

Who exactly is Dongtai Qixin? Why has it made two such massive investments within just one year? What does Dongtai Qixin’s entry into the PPS sector—characterized by extremely high barriers to entry—signify?

Figure PPS resin (Source: New Harmony)

The Leader Behind Taiqi New

To understand Dongtai Qixin, one must first be familiar with its affiliated company—Anhui TEDA New Materials Co., Ltd. (referred to as "TEDA New Materials," listed on the NEEQ under stock code: 430372).

Taida New Materials Co., Ltd., established in 1999 and headquartered in Huangshan, Anhui Province, is a high-tech enterprise specializing in heavy aromatic oxidation products. Its core products are trimellitic anhydride (TMA) and hemimellitic acid. TMA serves as a critical raw material for manufacturing eco-friendly plasticizers, high-end powder coatings, and advanced insulating materials. Though seemingly ordinary, TMA’s price trend in recent years has been anything but.

While achieving soaring performance, Taida New Materials' journey in the capital market has been fraught with setbacks. The company has repeatedly failed in its attempts to enter the capital market—failing twice in IPOs on the ChiNext and the Beijing Stock Exchange, until February 26, 2025, when it once again negotiated with Open Source Securities to terminate the Beijing Stock Exchange tutoring filing agreement.

In July 2025, Taida New Materials sold an industrial land-use right located in the Huangshan City Huizhou Chemical Industry Park to Huangshan Dongtai Qixin Technology Co., Ltd. for RMB 39 million—a land transaction that served as the critical step enabling the implementation of the Huangshan PPS project.

The person at the helm of both companies is Ke Bocheng, who serves as the chairman of both Anhui TaiDa New Material Co., Ltd. and Jiangsu DongTai QiXin Technology Co., Ltd.

This is the basic structure of the "Taida Group": a parent company that has been deeply involved in the chemical industry for more than two decades, accumulating considerable capital and manufacturing experience, as well as a newly established company specifically responsible for betting on the PPS new business direction.

Hardcore Strength! What Makes PPS Capable of Supporting Half the High-End Market?

Polyphenylene sulfide (PPS) is a high-performance engineering thermoplastic with excellent thermal stability, chemical resistance, dimensional stability, and inherent flame resistance. PPS can maintain its properties without significant degradation at continuous service temperatures of 200–240°C, making it suitable for high-demand application fields such as automotive, aerospace, electronics, and chemical industries. It has low hygroscopy, excellent electrical insulation properties, and can withstand solvents, fuels, and acids. PPS can be produced in different forms, including glass fiber or mineral reinforced composites, to enhance mechanical strength and toughness.

Image source: Napan

With these properties, PPS is commonly used in automotive engine compartment components, pump parts, electrical connectors, coatings, and filtration systems, and is also considered a potential core material for emerging applications such as actuator and sensor housings in humanoid robots.

Market data confirms the appeal of this sector. QYResearch indicates that the global polyphenylene sulfide (PPS) resin market size will be approximately $19.33 billion in 2025, and is expected to reach $26.99 billion by 2032, with a compound annual growth rate (CAGR) of 5.0% from 2026 to 2032. China is the world's largest PPS consumer, with high-end products still highly dependent on imports from Japan and the United States, highlighting a significant structural supply and demand imbalance.

The production barriers for PPS mainly stem from process complexity. The current mainstream synthesis route is the "sodium sulfide method," which involves a condensation polymerization reaction between p-dichlorobenzene (p-DCB) and sodium sulfide (Na₂S) under high temperature and high pressure. Globally, only three countries—the United States, Japan, and China—truly master the core technology for large-scale commercial production. PPS is categorized into two main types based on its physical form: "cross-linked" PPS (lower-cost, primarily used in filter bags, etc.) and "linear" PPS (high-end grades with better flowability, suitable for precision injection molding). Among these, linear PPS has higher technical barriers, and only a handful of companies worldwide can reliably supply it.

PPSFramework: Japan First, China urgently pursues.

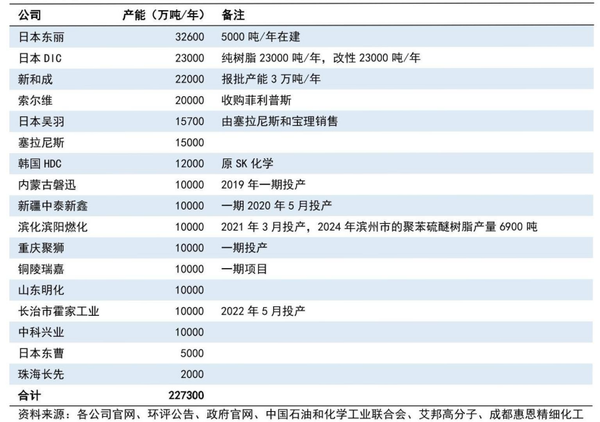

Currently, the global PPS production capacity is approximately 227,300 tons per year. Countries and regions such as Japan, South Korea, Europe, and the United States, which have a longer history of development in the PPS field, currently hold a leading position. In particular, Japan has a first-mover advantage in the PPS field, with Toray, DIC, and Kureha demonstrating strong competitive advantages in PPS brands, product quality, and cost.

It has long been the world's top producer. More importantly, Toray not only leads in production capacity but also has built a high technical barrier - it continues to expand production at its Japanese plants and will launch the world's first high-performance flexible PPS resin in February 2026, representing the current pinnacle of linear PPS technology.

DICCapacity of 23,000 tons per year, including 2,300 tons per year of pure resin and 23,000 tons per year of modified capacity. Japanese companies have concentrated layouts in this field. 、DICoutside, Japan Capacity: 15,700 tons/year (sold by Celanese and Polyplastics), Japan Capacity: 5,000 tons per year; the combined capacity of these Japanese companies exceeds 75,000 tons.

Domestic Leader, ZhejiangXinhechengWith an annual production capacity of 22,000 tons, it ranks third globally and is currently the only enterprise in China capable of stably mass-producing PPS resins in multiple specifications. In 2024, the capacity utilization rate reached 100%, and in November 2025, it launched a bio-based PPS product that has received international ISCC certification, with plans to expand the production capacity to 30,000 tons. Moreover,Chongqing Jushi, Shandong Binhua Binyang, Xinjiang Zhongtai XinxinCompanies such as these have all laid out production capacities at the 10,000-ton level, and the competitive landscape of the second tier in the domestic market has basically taken shape.

However, the domestic PPS industry still faces significant bottlenecks in its high-end development: high-end grades with low chlorine content and ultra-high molecular weight remain heavily reliant on imports from Japan, resulting in a low domestic substitution rate.

Tai Qi XinEntry into the market is Can re-bet ?

Dongtai Qixin's approach to entering the market is different from the expansion logic of traditional chemical companies—it does not iterate on existing capacity, but instead aims directly for the "world's largest single-unit capacity" from the start.

From the perspective of site selection logic, the two bases have distinct focuses. The Huangshan base relies on Taieda New Materials' existing land, park relationships, and chemical manufacturing experience, following a parent company incubation approach; while the Yundong Yangkou Port base holds greater strategic value. Yangkou Port is a key deep-water port, adjacent to the Yangtze River Delta industrial hinterland, with convenient access for chemical raw material imports and exports. Moreover, the local government is actively building a "wind, photovoltaic, storage, gas, and hydrogen" energy system, providing stable energy support for energy-intensive chemical projects.

More worthy of attention is TEDA New Materials’ industrial chain synergy value. TMA and PPS share certain linkages at the raw material stage—both involve deep processing of aromatic compounds. TEDA New Materials’ accumulated expertise in oxidation processes in the trimellitic anhydride (TMA) sector, along with its control over procurement channels for heavy aromatic feedstocks, could provide Dongtai Qixin with opportunities for resource integration at the upstream raw material stage of PPS (e.g., procurement of p-dichlorobenzene or equity participation).

Of course, questions remain. While the capacity planning is ambitious, the technology source is the most critical—and least transparent—aspect of this project. Publicly available information has not yet disclosed whether Dongtai Qixin adopts a specific technological route, whether it has licensed technology from external parties, or whether it has developed the technology independently—a key hurdle in the PPS field. Compared with capacity expansion, the barriers to entering the cross-linked PPS market are relatively low; several domestic enterprises have already achieved stable production. The true challenge lies in the continuous, stable production of linear, high-purity PPS, and in meeting the stringent requirements—such as low chlorine content and high melt flow—of high-end applications like electronic packaging.

Moreover, the time lag between capacity planning and market absorption is also a variable. According to data from Zhiyan Consulting, global PPS resin production capacity reached 210,000 tons per year as of 2024, while China’s PPS resin consumption rose steadily from 39,000 tons in 2020 to 56,000 tons in 2024. If Dongtai Qixin’s proposed 240,000-ton capacity is fully realized, it would create significant short-term overcapacity pressure; whether this will trigger a repeat of the price wars observed in other chemical sectors remains an industry concern.

Alternative acceleration, but high-end breakthrough is the key.

Regardless of whether Dongtai Qixin ultimately achieves its planned production capacity, this case itself has already sent a clear signal: the PPS sector is entering a new phase of intensive capital deployment by Chinese investors.

The logic driving this wave is not complex. As the penetration rate of new energy vehicles continues to rise, the PPS usage per vehicle also increases; humanoid robots are beginning to enter mass production expectations, and the demand for heat-resistant and insulating special engineering plastics has already been included in the industry research of many securities firms; 5G base stations and high-end electronic packaging are also releasing incremental demand. The expansion of domestic consumer demand, coupled with the policy orientation of import substitution, makes the long-term logic of the PPS track relatively clear.

According to the consulting data from the China Chemical Information Center, China's PPS self-sufficiency rate increased from 45% to 64% between 2020 and 2023. The significant improvement in self-sufficiency rate still sees China's PPS industry lagging behind Japanese veteran companies such as Toray and DIC in terms of overall process technology, modification and customization capabilities, and the depth of industrial chain cooperation with high-end users. The Chinese PPS industry is not short of the momentum for capacity expansion, but lacks the technical accumulation and customer validation required to tackle high-end linear grades.

Dongtai Qixin's emergence adds a new case study to this proposition: a company with capital accumulation, experience in chemical operations, and government resource support has chosen to enter the PPS market through sheer scale. Whether it can achieve technological advancement while ramping up production capacity remains the biggest question hanging over the project.

Editor: Lily

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Raw Material Supply Shortage! INEOS Phenol Declares Force Majeure on Phenol and Acetone Businesses

-

Lantiche Group To Shut Down Italian Adipic Acid Production Plant

-

Resin Market Trends Diverge: Buyers' Bargaining Advantage Hit by Geopolitical Uncertainty

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Strait of Hormuz Blocked Again, Supply-Demand Mismatch in Polyolefin Market Set to Intensify!