900,000-Ton-Per-Year Ethylene Plant Shut Down! ExxonMobil Reshapes Asia-Pacific Petrochemical Landscape

On May 22, 2026, ExxonMobil officially confirmed that its No. 1 steam cracker on Jurong Island, Singapore, which had been in operation for 24 years, had been shut down, affecting an annual ethylene production capacity of 900,000 tons.

I. Reconstructing the Incident: The Timeline Behind a Factory Shutdown

On May 21, 2026, a spokesperson for ExxonMobil confirmed the news to the public without disclosing the specific facility name: "We have shut down a chemical manufacturing plant that began operations in 2002. We will continue to work with our customers to meet their needs, leveraging our global asset base and product inventory. If market conditions improve, we have the capability to restart the unit."

The unit being shut down this time is ExxonMobil’s Singapore No. 1 steam cracker, with an annual ethylene capacity of 900,000 tonnes. It is the earlier-built and longer-serving of the company’s two steam crackers in Singapore. At present, the No. 2 cracker, with an annual capacity of 1 million tonnes, is still operating, but the site’s overall capacity has now been sharply reduced from 1.9 million tonnes to 1 million tonnes.

II. Why Now? A Long-Predestined Farewell

From the plan announcement in December 2025 to the official production halt in May 2026, none of this happened suddenly. To understand this time window, one needs to grasp the industry pressure formed by three sets of numbers.

(1) Profit collapse: the Asian naphtha route is no longer profitable

Naphtha cracking to ethylene is the core process route of the Singapore facility, but it is also its fatal weakness.

With high oil prices, naphtha costs are rising rigidly, while ethylene prices are being held down by weak demand. The spread remains persistently inverted, and every ton of ethylene produced is making a loss. In contrast, the profitability of the ethane route and the coal-to-chemicals route is much more favorable.

(II) Flooding the Market with Supply: China’s Capacity Expansion Breaks Through Regional Pricing

Alongside the cost disadvantage is the capacity shock from upstream.

According to industry data, China’s ethylene output reached 41.508 million tonnes in 2025, up 6.4% year on year (source: Huaan Securities, April 2026). China’s ethylene production capacity has reached 62 million tonnes per year, surpassing the United States to become the world’s largest ethylene producer, accounting for about 25% of global capacity.

This means that the aging plants that once supplied polyolefins and chemicals to the Asia-Pacific market are losing the market rationale for their existence. China is no longer merely a single consumption endpoint; it has also become the largest player among the competitors.

(3) Aging Installations: Natural Attrition over a 24-Year Service Life

No. 1 cracking unit was commissioned in 2002 and has now been in operation for 24 years. For a large-scale cracking unit, this represents a considerable service life—bringing with it higher maintenance costs, lower energy efficiency, and increasing pressure to meet carbon emissions regulatory requirements.

In its statement, ExxonMobil’s spokesperson used the term “deactivated” rather than “permanently shut down,” thereby preserving legal room to restart the unit. Industry observers, however, generally believe this is more of a diplomatic turn of phrase—in current market conditions, the likelihood of restarting a naphtha cracker is closely tied to the timeline for a reversal in the industry cycle, which does not look optimistic.

Three, Singapore is just the latest step! ExxonMobil's global subtraction logic.

The shutdown in Singapore is not an isolated incident but rather the latest move in a series of contraction actions.

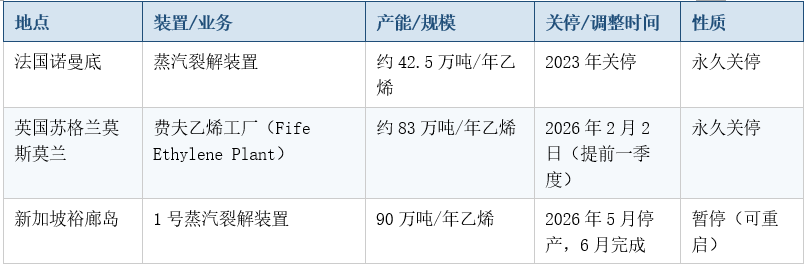

Overview of ExxonMobil’s Chemical Asset Closures/Adjustments in Recent Years

Source: ChemNet Chemical Industry Headlines

Three shutdowns, involving a combined ethylene capacity of about 2.15 million tons per year (France + UK + Singapore). This figure is equivalent to the annual output of a medium-sized integrated refining and petrochemical project. From France to the UK and then to Singapore, European ethylene assets have been completely cleared out, and the Asia-Pacific region has also begun a selective contraction.

But contraction has never been a one-way street. While making cuts, ExxonMobil is also working on a major expansion in Asia-Pacific.

4. Doubling Down on China! Why Invest $10 Billion in Huizhou, China?

On July 15, 2025, the ExxonMobil Huizhou Ethylene Project was officially put into operation in Daya Bay, Huizhou, Guangdong—this is the first major petrochemical project wholly owned by a U.S. company in China, with a total investment of over $10 billion (Source: Huizhou Municipal Bureau of Commerce, July 15, 2025).

Compared with the aging facilities in Singapore that are being shut down, the Huizhou project is of an entirely different scale.

Table: Core Indicators of the First Phase of the ExxonMobil Huizhou Ethylene Project

Source: Huizhou Municipal Bureau of Commerce Official Website (July 15, 2025); ExxonMobil Chemical China Official Website

It is worth noting that the Huizhou project is not an ordinary large-scale cracking complex—it targets the high-end differentiated products market. Its LDPE unit is described as the “world’s largest single-train LDPE unit,” its polypropylene product line is positioned toward “differentiated high-performance grades,” and it is supported by R&D capabilities serving the Asia-Pacific market. This stands in stark contrast to the outdated facilities being shut down in Singapore, which were primarily focused on supplying ethylene feedstock.

An industry researcher summed up this comparison quite precisely: China’s plant construction costs are only about 50% of those in the U.S. Gulf Coast, its industrial chain is complete, it enjoys policy support, and it is close to end markets—in Asia Pacific, there is no more cost-competitive location for new construction than China (source: Zhihu Plastic Helper, January 2026).

5. Retiring Aging Facilities: This Is Not Just ExxonMobil’s Story

ExxonMobil’s shutdown in Singapore reflects a broader industry landscape: capacity at the tail end of the old cost curve is undergoing a systemic purge under the dual pressures of oversupply and losses.

Taking Dow Chemical as an example: in 2025, net sales reached US$39.968 billion, down 7% year on year, and full-year net loss was US$2.444 billion (source: *2025 Ethylene Industry Review and 2026 Outlook*, March 2026). SABIC has shut down its 865,000 t/y ethylene cracker in the UK; Yeochun NCC in South Korea has announced an indefinite shutdown of its 470,000 t/y cracker. Industry estimates indicate that South Korea’s petrochemical sector still plans to cut naphtha cracking capacity by 2.7 million to 3.7 million t/y in the future (source: same as above).

On the other side of Asia, Japanese petrochemical companies are also bearing similar shocks — in the first quarter of 2026, Japanese steam crackers were affected by disrupted naphtha supply due to the situation in the Middle East and the elimination of outdated units, involving nearly 1.75 million tons/year of capacity (source: Baijiahao, “Comprehensive Deep Dive into Japan’s Bulk Chemical Industry in Q1,” April 29, 2026).

This is not the predicament of a single company, but a systemic retreat of the naphtha route on a global scale under the multiple pressures of ethane-based, coal-based, and newly built integrated plants.

VI. Implications for Plastics Industry Practitioners

ExxonMobil characterized the shutdown as “part of its global asset optimization strategy, focusing on core assets with stronger competitive advantages.” What it is building in Huizhou, China, is precisely a model that defines the next generation of “core assets” — larger in scale, higher-end in products, stronger in supporting R&D capabilities, and more competitive in construction costs. For participants in China’s plastics and chemical industry chain, understanding this shift in the standards for “core assets” will help assess the future direction of raw material procurement and technological cooperation.

Whether it is the shutdown of the old plant in Singapore or the anchoring of the new plant in Huizhou to high-performance polyolefin grades, the message conveyed is the same: price competition in commodity materials has become a pure cost war, while premiumization and differentiation are the structural way out. While domestic plastics downstream enterprises are bargaining with raw material procurement costs, they also need to consider how to enhance their capacity to absorb high-performance materials on the product side, so as to take a proactive position in the restructuring of the supply chain.

Editor: Lily

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Raw Material Supply Shortage! INEOS Phenol Declares Force Majeure on Phenol and Acetone Businesses

-

Lantiche Group To Shut Down Italian Adipic Acid Production Plant

-

Resin Market Trends Diverge: Buyers' Bargaining Advantage Hit by Geopolitical Uncertainty

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Strait of Hormuz Blocked Again, Supply-Demand Mismatch in Polyolefin Market Set to Intensify!