Automotive industry profit margins continue to plummet: Who Is Really Making the Money?

In 2026, the Chinese auto market appears lively on the surface, but its core is cold.

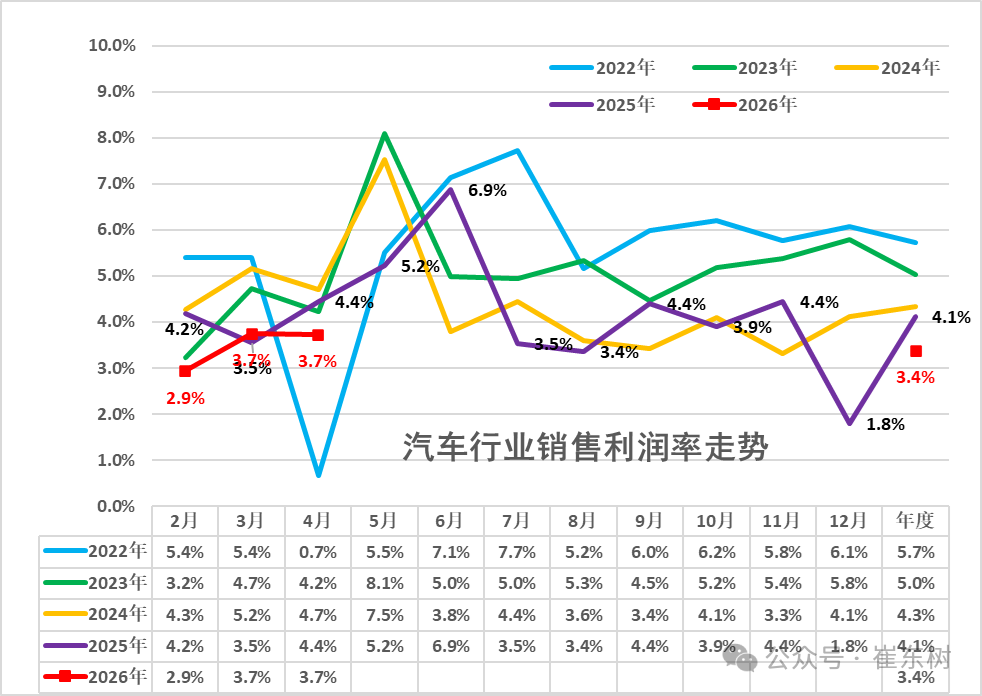

On the bustling side, there are more and more green-plated cars on the road, the penetration rate of new energy vehicles continues to rise, and new car launches are coming one after another, making the market look vibrant. On the cooler side, however, is the difficult reality of profitability hidden beneath the glamorous surface. According to the latest data shared by Cui Dongshu, Secretary-General of the China Passenger Car Association, in January-April 2026, the profit margin of the automotive industry further declined to 3.4%.

Image source: Cui Dongshu (same below)

Don’t be fooled by the increasing number of new cars on the streets—companies and their partners in the supply chain are actually feeling the pinch. While revenue only grew by 1.1%, costs rose by 2%, directly causing a 17% plunge in profits. This isn’t just a numbers game on paper; it’s a “red light” warning about the health of the entire industry ecosystem.

The figure of 3.4% is not unprecedented when viewed in historical context. Data shows that it dropped to 3.2% in February 2023, reached 3.4% in September 2024, fell to 3.3% in November 2024, and plummeted to a shocking 1.8% in December 2025. In other words, the profit margins in the automotive industry have been struggling around the 3% level in recent years, occasionally dragged into deeper depths.

When expansion in scale can no longer translate into real cash, we can’t help but ask: in this vast industrial chain, who is siphoning off the profits?

The automotive manufacturing industry, caught in the squeeze from both ends, has fallen into a predicament of increasing revenue but not profits.

The current situation of the automotive industry can be described as "caught between a rock and a hard place." Cui Dongshu stated that recently, as the production scale of the car market has expanded, the PPI has risen, leading to a surge in profits for upstream non-ferrous metals and petroleum industries. However, end users are severely hesitant to purchase cars due to various factors. The manufacturers in the middle are facing unprecedented pressure.

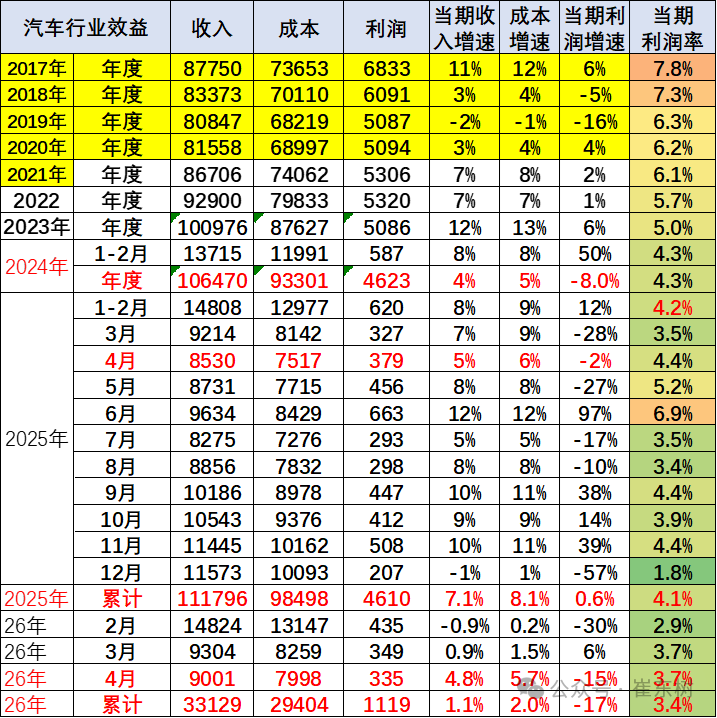

First, let’s look at the “revenue vs. expense” gap. According to data shared by Cui Dongshu, from January to April 2026, the total revenue of the automotive industry reached 3,312.9 billion yuan, a year-on-year increase of just 1.1%. This slight growth was achieved amid fierce competition among major brands, with relentless price cuts, feature wars, and service wars. However, the cost was also severe: total costs during the same period reached 2,940.4 billion yuan, up 2% year on year. As a result, already thin profits were rapidly eroded.

This explains why sales figures may still look quite good, yet a look at the profit statement reveals that many companies are actually “making noise at a loss.” In particular, the traditional fuel vehicle segment is under immense pressure amid the wave of new energy transition: it must both maintain market share through price wars and invest massive sums in developing new technologies, burning cash on both fronts, so it is only natural that profits can hardly bear the strain.

Cui Dongshu's shared data clearly reveals this long-term downward trend. In 2014, the sales profit margin of the automotive industry could still maintain a high level of around 9%. By 2024, this figure had dropped to 4.3%, continuing to decline to 4.1% in 2025, and by the first four months of 2026, it had already fallen to 3.4%. Although the single-month performance of 3.7% in April was slightly better than the first quarter, looking at the longer timeline, profit margins around 3% have become the norm, with the figure of 1.8% in December 2025 hitting rock bottom.

One noteworthy detail is the change in profit per vehicle. Data shows that from January to April 2026, the average revenue per vehicle across the automotive industry chain was RMB 342,000, up 6% year on year, while the average cost per vehicle also rose to RMB 303,000, up 6.93% year on year. As cost growth outpaced revenue growth, the average gross profit per vehicle across the industry chain fell to just RMB 12,000, down 12.1% year on year. This means that with each car sold, the gross profit automakers can actually pocket is shrinking rapidly.

It is worth noting that in the entire downstream industrial sector, the automotive industry has one of the lowest profit margins. From January to April, the average profit margin of downstream industrial enterprises was 6.1%, while the automotive industry only reached 3.4%, less than half of the average level. Compared to "profit cows" like alcohol, tobacco, and pharmaceuticals, manufacturing cars has become less rewarding—more resources are invested, greater pressures are borne, yet the profits obtained are quite meager.

Upstream profits have surged and battery costs remain high—who is taking the profits?

Under the background of continuous pressure on profits in the complete vehicle segment, a natural question arises: where is the money flowing? From the perspective of profit distribution in the industry chain, it is indeed the upstream mining sector and the power battery segment that occupy a larger share.

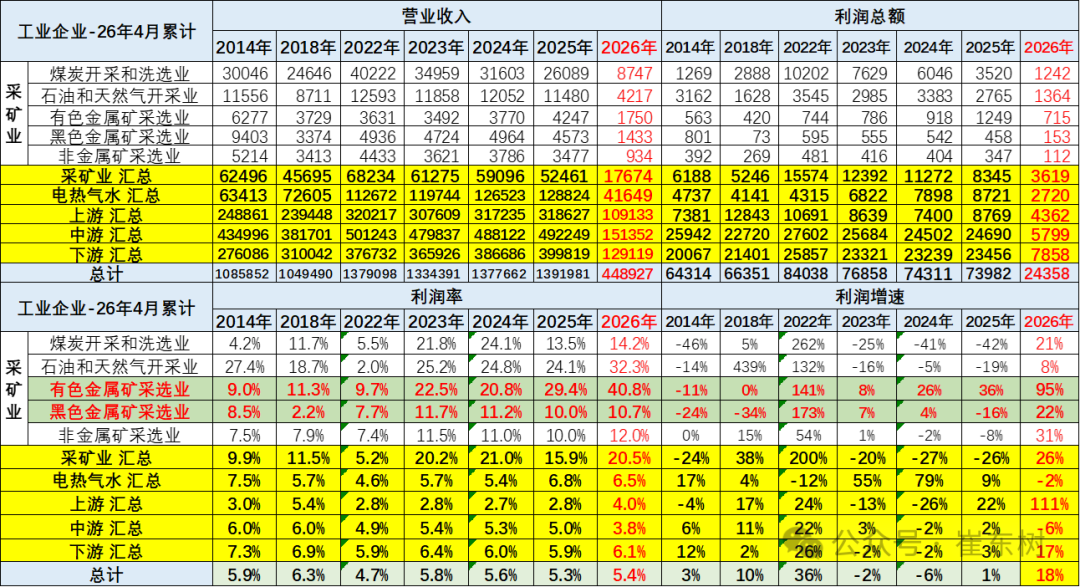

Upstream mining industries are "quietly making a fortune." In his analysis, Cui Dongshu pointed out that from January to April 2026, profits in the mining industry increased by 26% year-on-year, with the profit margin remaining at an extremely high level of 20.5%. In particular, the non-ferrous metals sector, which is closely related to the automotive industry, saw its profit margin surge by 40.8%, while the petroleum industry grew by 32.3%. The high prices of bulk commodities such as non-ferrous metals and petroleum have directly pushed up the basic costs of automobile manufacturing.

NIO CEO Li Bin mentioned in a recent "NIO ES9 Media Face-to-Face" communication that since the beginning of this year, the prices of raw materials, including nickel, cobalt, and lithium carbonate, have increased, raising the cost of a vehicle by over 10,000 yuan. He pointed out that the impact of commodities and memory chips affects not only the automotive industry but also faster-growing and wealthier sectors, leaving car manufacturers with little bargaining power. Since memory prices have risen this year and have not yet decreased, the cost increases from raw materials are unlikely to drop in the short term, and these costs must be absorbed by the companies themselves.

This trend of profits concentrating upstream essentially creates a "squeeze" effect from upstream to midstream and downstream. When raw material prices surge, the manufacturing sector, which is in the midstream, often has limited bargaining power and has to bear most of the cost pressure. It's like a bakery; if the prices of flour and sugar rise significantly, the bakery owner may not be able to directly raise prices and can only absorb the costs for a while.

The issue of profit distribution in the battery segment is more direct. Cui Dongshu pointed out that lithium battery export prices continue to fall, while domestic battery prices have surged. The problem of automakers not producing batteries is serious, and their profits may continue to decline.

This statement gets straight to the heart of the issue. The logic is as follows: although export prices for lithium batteries are declining, domestic battery procurement prices remain high due to strong domestic demand and the pass-through of upstream costs such as lithium carbonate.For most car manufacturers without self-developed battery capabilities, battery procurement is a fixed expense that usually accounts for 30%-40% of the total vehicle cost, or even higher.

This means that a considerable portion of a vehicle’s profit margin is effectively locked in by battery costs. This also explains why leading automakers such as BYD, Great Wall, Geely, and GAC Aion are accelerating the construction of their own battery plants. Through vertical integration, automakers can to some extent regain control over costs and profit margins.

Another noteworthy signal is that when terminal market competition intensifies and price wars continue, automakers have limited room to raise prices, while upstream raw material and battery costs remain relatively rigid. This “squeezed from both ends” situation makes automakers’ profit statements quite fragile. If sales fluctuate, or if raw material prices rise further, some companies that are already on the edge of break-even may face greater financial pressure.

So, is the decline in profits entirely attributable to upstream suppliers? The answer is probably not that simple. In fact, there are two other pressures eroding automakers’ profit margins: first, the endless price war—companies are forced to “trade price for volume” in a bid to capture market share, with profits constantly squeezed by cutthroat competition; second, the strategic costs brought about by the shift to new energy vehicles—massive R&D spending is booked as current costs, yet the returns will only come in the future. It is the combination of these three pressures that has created the current low-profit-margin predicament.

Farewell to "involution-style" growth, how to find new profit points?

Faced with persistently declining profit margins and profits being squeezed by upstream and downstream players, the automotive industry stands at a crossroads. The old, extensive growth model of “trading price for volume” and sacrificing profits for market share has clearly reached its limit. As the country continues to advance its anti-involution efforts, the industry is also seeking new profit drivers.

The calls to “push back against excessive cutthroat competition” are by no means unfounded. Since 2025, from the Ministry of Industry and Information Technology to the Ministry of Commerce, and on to industry associations across various regions, authorities have been guiding industries in different ways to avoid disorderly price wars. This is because people are increasingly realizing that prolonged low-price infighting will only weaken companies’ capacity for R&D and innovation, ultimately harming the competitiveness of China’s automotive industry as a whole.

Specifically, as for how to break the deadlock, first, the call for “equal rights for fuel and electric vehicles” is becoming increasingly realistic. Over the past few years, new energy vehicles have enjoyed a series of policy benefits, including purchase tax exemptions and preferential road access. While these were necessary during the market cultivation stage, the penetration rate of new energy vehicles is now already at a relatively high level, and the market has developed a certain degree of self-sustaining momentum.

Promoting equal treatment for gasoline vehicles and new energy vehicles, so that they can compete on a level playing field, can on the one hand stabilize the foundation of the gasoline vehicle market and ease the transition pains of traditional automakers; on the other hand, it can compel new energy vehicle companies to compete on the basis of product strength rather than policy dividends, thereby eliminating outdated capacity that survives on subsidies and allowing the fittest to prevail. Cui Dongshu has previously emphasized many times that stabilizing gasoline vehicle consumption and promoting vehicle scrappage and replacement are crucial to the healthy development of the industry.

Second, automakers need to place greater emphasis on controlling their core supply chains. Judging from the choices of some leading automakers, future competition will not only be a contest of vehicle models and intelligence, but also a battle of supply-chain control and cost-management capabilities. BYD’s vertically integrated model, for example, has effectively reduced costs through in-house battery development, offering a viable path for the industry. As a result, developing batteries in-house and vertically integrating the industrial chain are becoming strategic options for an increasing number of leading automakers.

Of course, there are still differing views within the industry. Some automakers believe the external supply chain is already sufficiently mature, and the return on investment for in-house R&D remains to be proven. What is certain, however, is that how to strike the right balance between control over the battery segment and return on investment will be a question every automaker must answer.

Furthermore, the focus is shifting from a “price war” to a “technology war” and a “value war.” As lithium carbonate prices return to rational levels and battery technology matures, the next major wave in the automotive industry will inevitably be intelligence. High margins have never come from simply piling on features, but from delivering a one-of-a-kind technological experience. Whether it is the real-world deployment of intelligent driving or the building of an intelligent cockpit ecosystem, whoever can create new revenue streams through software and services will be able to break free from the low-margin trap of merely selling hardware.

Finally, consumers at large also need to recognize a reality: extremely low prices are often unsustainable. If an industry remains in a state of razor-thin margins or even losses for an extended period, product quality, after-sales service, and continued investment in research and development will all become difficult to sustain. Only by allowing companies to earn reasonable profits can the entire ecosystem maintain a positive cycle.

The data shared by Cui Dongshu once again brings to light a recurring issue in the automotive industry: while scale is increasing, profits are declining. A profit margin of 3.4% is not the most extreme in recent years, but the fact that it has been hovering around the low level of 3% for a long time indicates that this is not an occasional fluctuation, but a structural predicament.

For automakers with true foresight, the real moat is not a few thousand extra units on the sales charts, but autonomous control over core technologies—whether battery cells, intelligent driving algorithms, or a brand premium capable of weathering economic cycles. Whoever can build their own advantages in these dimensions is more likely not only to survive the second half of the race, but to thrive in it.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Raw Material Supply Shortage! INEOS Phenol Declares Force Majeure on Phenol and Acetone Businesses

-

Lantiche Group To Shut Down Italian Adipic Acid Production Plant

-

Resin Market Trends Diverge: Buyers' Bargaining Advantage Hit by Geopolitical Uncertainty

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Strait of Hormuz Blocked Again, Supply-Demand Mismatch in Polyolefin Market Set to Intensify!