May Car Resale Value: More Inventory, but Prices Fell

On June 2, the China Automobile Dealers Association and Jingzhen Gu jointly released the “May 2026 China Automobile Residual Value Research Report.” The data show that in May, the volume of online vehicle listings continued the previous recovery trend, edging up slightly month on month and also coming in slightly higher year on year than in the same period last year.

The main drivers behind this market rebound are the combined effects of the consumption boom during the May Day holiday and the trade-in subsidy policy. The backlog of new car orders accumulated earlier was released in May, effectively stimulating users’ replacement demand, which in turn brought a large number of used cars into the market.

In contrast to the rebound in vehicle supply, residual value retention rates across all vehicle segments have generally come under downward pressure. The association noted that although prices of some new energy vehicle brands have recently adjusted downward, the fundamentals of the used-car market are still dominated by traditional fuel-powered vehicles. The ongoing price-cut competition in the new fuel-vehicle market has directly dragged down the overall performance of the used-car market.

This “higher volume, lower price” structural pattern precisely confirms one of the report’s judgments: China’s new energy vehicle industry is moving away from the crude growth phase of “trading price cuts for sales growth” and entering a new cycle of value-based competition centered on technology, products, and services.

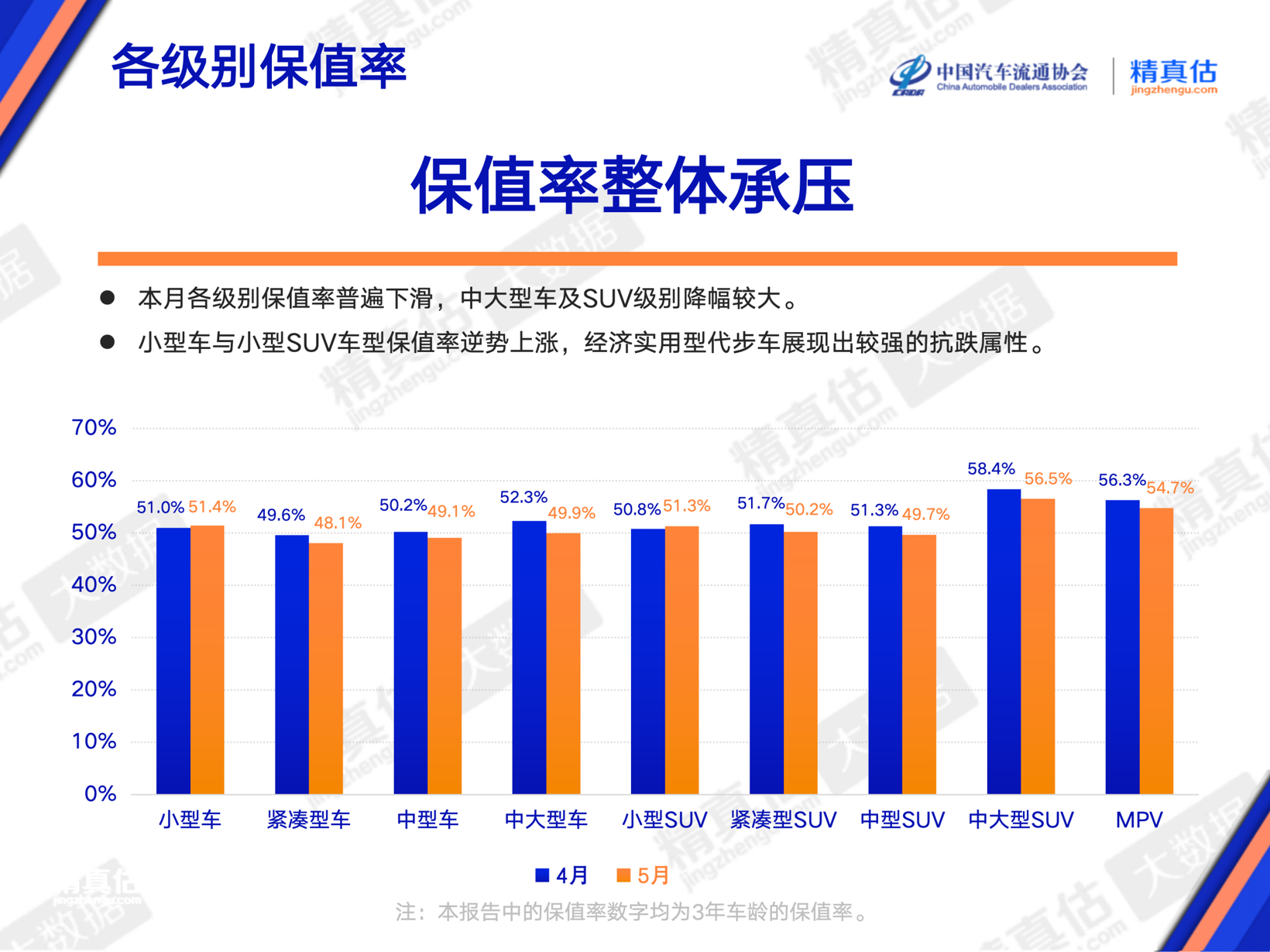

Small essential vehicles resist price drops against the trend, while mid-to-high-end models face significant pressure.

Against the backdrop of an overall decline in residual value rates, the trends across different subsegments have shown clear divergence.

The report shows that the mid-to-high-end market, represented by midsize and large sedans as well as midsize and large SUVs, has been hit the hardest by new car price cuts, with residual values seeing some of the largest declines. In contrast, small cars and small SUVs emerged as the only segments to rise against the trend this month.

Image source: China Automobile Dealers Association (same below)

The association analyzed that this contrast mainly stems from two points: first, the guide prices for these types of vehicles are relatively low; second, in the current environment of high oil prices, low-energy (including pure electric) commuter cars are more favored by practical buyers. The changes in usage scenarios and supply-demand relationships provide solid support for the resale value of essential commuter models.

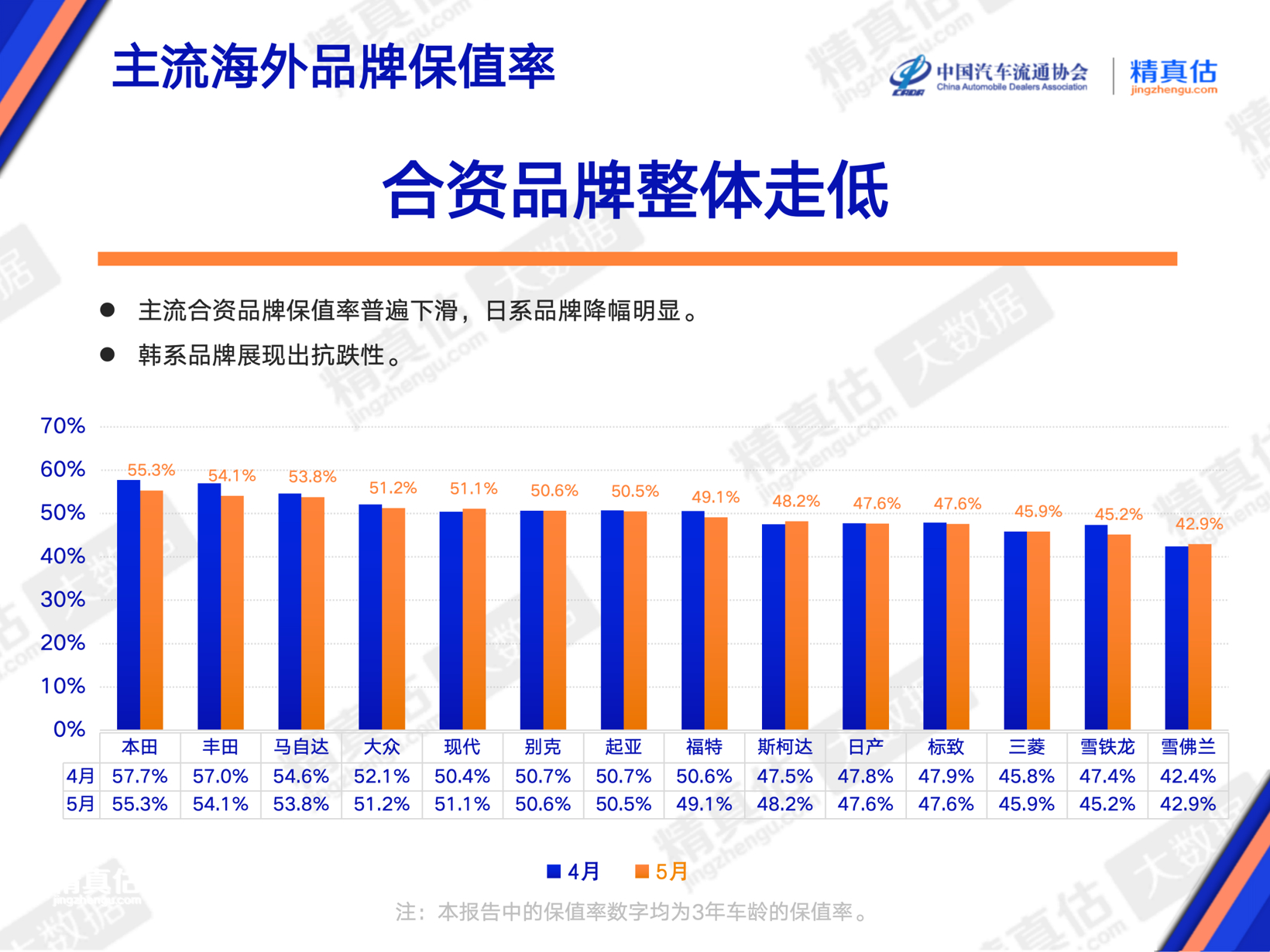

From a brand lineup perspective, traditional luxury brands and mainstream joint-venture brands are generally facing pressure. The report shows that in May, the overall residual value rate of luxury brands declined significantly, and traditional fuel-powered luxury brands were under pressure across the board.

The report suggests that behind this, it is not only the impact of new car price wars, but more importantly, the “off-season effect” has begun to take hold. After entering May, the turnover cycle for used cars lengthened, and dealers generally worried that “the inventory hasn’t been cleared yet, and new cars have already been discounted again.” In order to leave themselves a safety margin, they proactively lowered the prices at which they acquired used cars, and this in turn amplified the overall decline in resale values.

The situation for joint venture brands is also not optimistic. In the Japanese camp, leading brands like Honda and Toyota have seen a decline in their resale value. The loosening of the new car price system has directly compressed the original premium capability of Japanese cars in the used car market.

However, among Korean brands, Hyundai has shown a certain degree of resilience against price declines. The report points out that although Hyundai’s presence in the new car market has weakened somewhat, in the used car segment its absolute prices are already at a low level. As a result, by virtue of its high cost performance and solid mechanical quality, it better meets the commuting needs of pragmatic users in the current high-fuel-price environment.

The self-owned brand new energy sector stabilizes, and technology-driven brands demonstrate residual value resilience.

Against the backdrop of overall market pressure, the performance of domestic brands emerged as a highlight of the report.

The report shows that domestic brands represented by GAC Trumpchi and Tank still remain firmly at the forefront. Behind this leading advantage is a combination of product reputation, quality stability, and user loyalty, while the dominance of fuel-powered vehicles in distinctive niche markets remains unshaken.

The more noteworthy changes come from the new energy sector.

The report clearly points out that the transition to electrification has become a key variable driving the increase in residual values. In May, independent new energy brands represented by Denza, BYD, and NIO continued to show improving residual values. This is interpreted as a clear signal that consumer acceptance of used electric vehicles from independent brands is rapidly increasing.

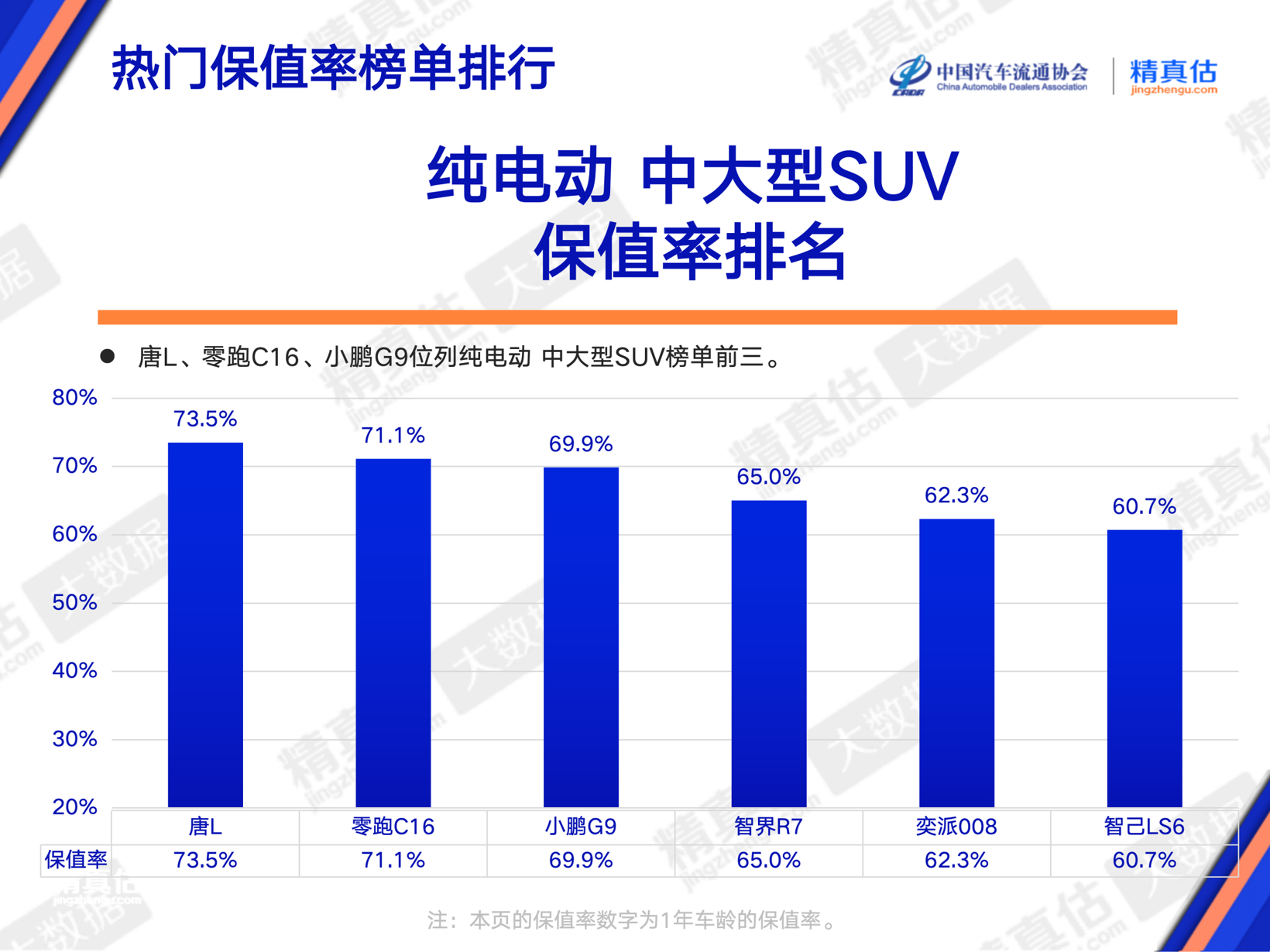

From the specific rankings, in the pure electric mid-to-large SUV market, the Tang L ranks first on the list. In the plug-in hybrid SUV market priced above 500,000 yuan, the Wenjie M9 also holds the top position. In the domestic pure electric compact SUV market, the Yuan PLUS ranks first on the list.

In addition to price data, the report also captured a policy signal that is favorable to the long-term development of the used new-energy vehicle market. As the implementation of the "Notice on Carrying Out the 2026 New Energy Vehicle Safety Hazard Inspection Work" advances, industry regulation is moving into deeper waters of "full life-cycle, whole-chain" oversight. Strict exit and penalty mechanisms—such as direct revocation of product announcements—will compel automakers to fully shoulder their primary responsibilities.

In the long run, the passive enhancement of quality and safety standards for new vehicles will provide the used car market with higher quality and more reliable vehicle sources. This will fundamentally alleviate consumers' "safety anxiety" regarding used electric vehicles and lay a more solid trust foundation for the large-scale and standardized circulation of used new energy vehicles.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Raw Material Supply Shortage! INEOS Phenol Declares Force Majeure on Phenol and Acetone Businesses

-

Lantiche Group To Shut Down Italian Adipic Acid Production Plant

-

Resin Market Trends Diverge: Buyers' Bargaining Advantage Hit by Geopolitical Uncertainty

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Strait of Hormuz Blocked Again, Supply-Demand Mismatch in Polyolefin Market Set to Intensify!