[pe daily review] crude oil plunge drags down costs, spot prices weaken across the board, future market under pressure

I. Today’s Summary

Geopolitical easing has weighed on oil prices, sending international crude sharply lower. Expectations of progress in U.S.-Iran peace talks have risen, easing market fears over crude supply shortages. The NYMEX July contract for crude oil fell 3.40%, and the Brent August contract dropped 2.97%, significantly weakening cost support for upstream polyethylene.

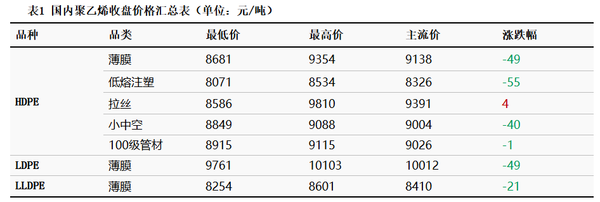

The domestic PE spot market as a whole trended downward, with differentiation among product types. HDPE fluctuated within a range of -55 to 4 yuan/ton, LDPE film was uniformly reduced by 49 yuan/ton, and LLDPE film dropped by 21 yuan/ton. Downstream buyers only purchased to meet immediate needs, transactions were sluggish, and traders adopted a wait-and-see attitude.

LLDPE futures weakened in tandem, and the spot-futures basis narrowed slightly. The number of idled industry units declined, leading to a modest increase in supply. Oil-based producers remained deeply loss-making, while coal-based producers enjoyed substantial profits. Market bearish sentiment across the industry strengthened month on month.

Core weekly data such as inventory, production, and capacity utilization rate will be released successively. There are expectations of inventory accumulation in factories, and there are signs of weakening downstream operations, making it difficult for the supply and demand fundamentals to improve.

II. Spot Overview

(I) Spot Quotations and Transactions by Category

Today, the overall spot polyethylene market shifted downward, with mainstream prices falling mainly by RMB 20–55/ton, while only HDPE raffia saw a slight increase of RMB 4/ton, and there was no concentrated restocking activity in the market.

HDPE showed significant divergence among sub-segments: low-melt injection molding saw the largest decline, with the mainstream price at RMB 8,326/ton, down RMB 55; film-grade mainstream prices fell RMB 49 to RMB 9,138/ton; small hollow products were lowered RMB 40 to RMB 9,004/ton; 100-grade pipe materials were nearly flat, down only RMB 1; while raffia edged up to RMB 9,391/ton, supported by limited targeted rigid demand.

The LDPE market is weak across the board, with the mainstream film quotation at RMB 10,012/mt, down RMB 49 in a single day. Downstream packaging and coating sectors are making small-lot purchases based on immediate needs.

LLDPE film mainstream price is RMB 8,410/ton, down by RMB 21. As the basic raw material for agricultural film and general packaging, end-user order volumes remain limited in the off-season.

(2) Futures Market Performance and Basis Performance

The LLDPE main contract traded weakly and range-bound during the day, opening at 7,888 yuan/ton and closing at 7,875 yuan/ton, down 50 yuan from the previous settlement. Trading volume for the day was 559,100 lots, and open interest stood at 368,500 lots, with overall capital activity remaining stable. The spot-futures basis for the current contract was 225 yuan/ton, narrowing by 7 yuan from the previous working day, indicating that spot prices were slightly more resilient than the futures market. Data source: Longzhong Information polyethylene basis trend data.

(III) Unit Scheduling and Production Profit

The overall plant shutdown rate on the supply side was 17.70%, down from 19.00% the previous day, indicating an increase in overall supply release. The production share of linear film was 25.20%, below the annual average; the production share of low-pressure pipe materials was 12.30%, significantly above the annual average, while the operating rates of low-pressure raffia and hollow grades were slightly below the normal annual average.

Cost-profit divergence is stark: oil-based PE production costs 9,308 yuan/ton, with a loss of 1,108 yuan per ton, putting pressure on refinery shipments; coal-based production costs only 6,938 yuan/ton, yielding a profit of 1,312 yuan per ton, and low-priced coal-based supplies continue to put pressure on market prices.

(4) Market Practitioners’ Mindset

This week's sentiment survey shows that the bearish proportion is 43.1%, an increase of 3.5 percentage points compared to last week; the bullish ratio is only 3.5%, a slight increase of 1 percentage point; over half of the participants chose to remain neutral, with a proportion of 53.5%, a decrease of 4.5% week-on-week. After completing a round of small-scale restocking, downstream factories have slowed down their purchasing pace, with finished product shipments not being smooth and the willingness to procure raw materials continuing to decline.

III. Price Forecast

1. Overall market outlook for tomorrow

Considering multiple factors including costs, supply and demand, and market sentiment, domestic polyethylene is expected to continue its downward trend on June 11, with overall market prices falling by around 50 yuan per metric ton.

Supply side: In the short term, several shutdown units are planned to restart, and the industry’s operating rate continues to decline. High operating rates for linear and low-pressure pipe-grade products offset the production cuts from maintenance shutdowns. Overall supply remains ample, with no obvious bullish support from tighter supply.

Demand side: Today's downstream stage inventory replenishment is basically coming to an end, and the purchasing activity is expected to significantly decline tomorrow. The end users are maintaining minimal production based on essential needs, and there is insufficient willingness to stock up in bulk, making it difficult to increase transaction volume.

Cost-wise: the sharp decline in international crude prices has weakened feedstock support. Loss-making oil-based producers have an incentive to cut prices to move cargoes, and low-priced coal-based supplies with high margins are suppressing overall quotations.

On the sentiment front, bearishness is intensifying. Most traders are cutting prices and selling off cargoes in line with the market to hedge risks, while holders lack confidence in maintaining firm offers, and a wait-and-see mood is dominating the market.

2. Volatility differences by category

HDPE: Low melting point injection molding, hollow, and film follow the market decline of 45-55 yuan; wire drawing is supported by slight demand, with the decline narrowing to 10-20 yuan; the demand for 100-grade pipes remains stable, with fluctuations controlled within 10 yuan.

LDPE: Demand remains somewhat weak. Tomorrow’s decline is expected to be close to the average, with a projected decrease of RMB 45–50/ton.

LLDPE: Futures market weakness dragged down spot prices, and the off-season for agricultural film provided no support, resulting in a decline of 40-50 yuan/ton.

3. Risk Warning

If geopolitical tensions between the U.S. and Iran escalate abruptly overnight, international oil prices could rebound quickly, slightly easing the market’s pessimistic sentiment, and the decline in PE may have room to narrow. On Thursday this week, key weekly data including production, maintenance volumes, and sentiment surveys will be released in a concentrated manner; after the data are published, the pace of the market may undergo a slight correction. This forecast is based solely on fundamental logic analysis and does not constitute any trading or investment advice.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Government's Triple Action, Enterprises' Three Arrows in Five Days, Semiconductor Reshuffle! What Signal Does Japan's Chemical Industry Release?

-

Name change without tax change: POM Anti-Dumping Duty Rate Inheritance Implemented

-

Fire breaks out at jiangsu meiside!

-

Ethylene: Production Capacity Accelerates Expansion, Global Industry Landscape Is Being Reshaped