Revenue shrinks by $30 billion, yet profits hold steady: Hengli Petrochemical’s Countercyclical Financial Report Reveals the “Antifragile” Logic of a Chemicals Giant

On April 14, Hengli Petrochemical (600346) disclosed its 2025 annual report as scheduled. Behind this substantial annual report, a set of figures stood out for their intriguing comparison: revenue fell from 236.2 billion yuan in 2024 to 200.986 billion yuan in 2025, a decrease of 14.63%; however, the net profit attributable to shareholders slightly increased from 7.044 billion yuan to 7.075 billion yuan, and the core earnings after deducting non-recurring items also saw a year-on-year increase of 14.21%.

Revenue declined by over RMB 30 billion, yet profit managed a slight increase—not a numbers game, but a true reflection of a leading integrated refining and petrochemical giant actively optimizing its structure, strengthening management, and prioritizing quality amid an industry-wide downturn.

One, understand"Revenue Reduction, Profit IncreaseIt's not accidental, it's structural.

To understand this financial report, it is essential to understand Hengli Petrochemical's industrial chain logic.

Crude oil enters the process, undergoes refining and processing to produce basic petrochemicals such as PX (para-xylene) and benzene; PX is then converted into PTA (purified terephthalic acid); PTA is polymerized with ethylene glycol to produce polyester products, including polyester filament, bottle-grade chips, films, and engineering plastics. The length of this integrated chain determines Hengli's resilience under pressure.

In 2025, this supply chain experienced a favorable cost adjustment: the international crude oil price level continued to decline throughout the year, which was a real cost benefit for Hengli, which processes 20 million tons of crude oil annually.

Image Source: Hengli Petrochemical

The financial report data confirms this assessment.The company's overall gross profit margin increased from 9.85% in 2024 to 13.14%, rising by 3.29 percentage points; the net profit margin also rose from 2.99% to 3.52%. The decline in revenue was largely due to the downward transmission of raw material prices to product prices (price and volume divergence, high price with low volume). However, the decline in cash expenses exceeded the decline in revenue, leading to an improvement in profit quality.

In terms of profitability, Hengli Petrochemical's net cash flow to net income ratio reached 4.4x, ranking among the highest in the petrochemical industry. This metric is often regarded as a "litmus test" for earnings quality. In 2025, the company's net cash flow from operating activities amounted to RMB 31.122 billion, an increase of 36.90% year-over-year, setting a new record high. This phenomenon is relatively rare in the petrochemical industry, as declining revenues typically coincide with deteriorating cash flow, yet Hengli Petrochemical has achieved a breakthrough in cash flow despite adverse conditions.

II. The Three Major Sectors Show Divergent Trends

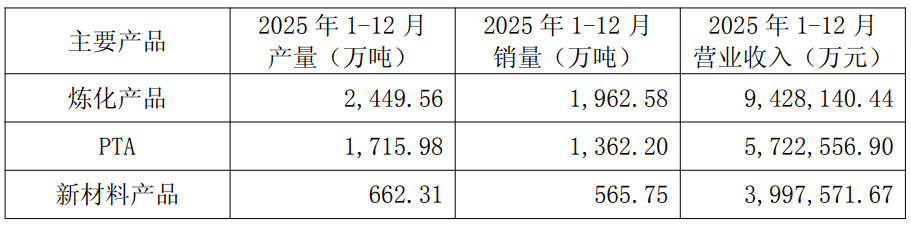

Hengli Petrochemical’s main businesses are divided into three segments: refining and petrochemicals, and PTA., polyesterThe performance of the three entities in 2025 reflects the varying temperatures across the entire petrochemical industry chain.

Table: Three Main Business Segments of Evergrande Petrochemical (Source: Evergrande Petrochemical Announcement)

Refining: The Most Profitable Link

The refining and chemical segment generated revenue of RMB 94.281 billion, with a gross margin of 20.91%, the highest among the three business segments. Key product output includes: 5.2 million tons of PX, 2 million tons of benzene, 1.8 million tons of fiber-grade ethylene glycol, 850,000 tons of polypropylene, and 720,000 tons of styrene annually.

The Dalian Changxing Island 20-million-ton-per-year integrated refining and petrochemical complex has significantly benefited from the "crack spread" during periods of low crude oil prices, leveraging its scale advantages and integrated synergies.

Notably, three companies within the Hengli (Dalian Changxing Island) Industrial Park have consecutively received the national Energy Efficiency "Leader" award for four years. Against the backdrop of mounting pressure to achieve "dual carbon" goals, leading energy efficiency rankings not only serve as a moat for policy benefits but also provide a competitive advantage in future carbon allowance trading.

PTAThe world's largest production capacity, but very thin profit.

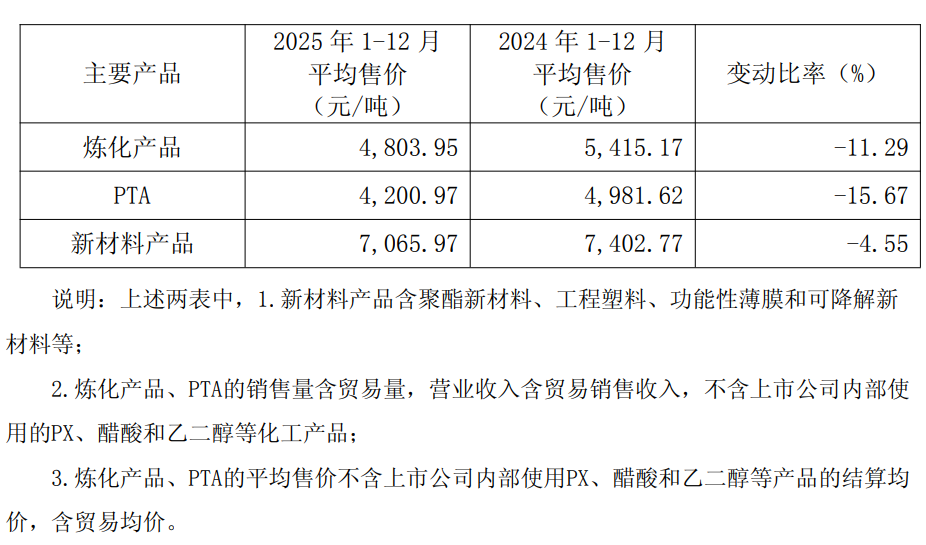

PTA sector is the area where Hengli has the most say — with an annual capacity of 16.6 million tons, it is the largest in the world, no comparison. However, PTA prices remained at the lowest level in three years in 2025, fluctuating in a "W" shape throughout the year, with the average price in East China ranging between 4,300 and 5,200 yuan per ton, experiencing significant volatility.

In 2025, the PTA business segment achieved operating revenue of RMB 57.23 billion, with a gross margin of 4.8%, the lowest among the company’s three major business segments. The company owns and operates world-leading PTA production capacity, reaching 16.6 million tons per year in 2025, making it the most technologically advanced and cost-competitive PTA producer in the industry. In 2025, PTA industry maintenance shutdowns increased, and enterprises alleviated supply-demand pressure through production cuts and temporary shutdowns. In September and October, the PTA industry held two “anti-competition” consultations, during which leading enterprises took the initiative to reduce output, sending a signal of industry self-discipline; consequently, product profitability improved.

Polyester: The Most Growth-Driven Segment

The polyester products segment generated revenue of RMB 39.976 billion with a gross margin of 7.35%. While this gross margin is not particularly impressive in absolute terms, taking a broader perspective reveals that polyester new materials represent the most critical growth engine for Hengli over the next decade.

In the downstream new materials sector, Hengli Petrochemical has continuously broken through technological bottlenecks, particularly in emerging fields such as functional film materials and high-performance engineering plastics. Kanghui New Materials has successfully overcome production bottlenecks for polarizer protective base films, raising the premium-grade product yield from 30% to 90%. Additionally, the company has developed high-value-added products including 0.8% low-haze in-line silicone-coated window films and food-contact-grade PBT resin. These innovations have not only enhanced product competitiveness but also created new growth drivers for the company.

These breakthroughs signify Hengli Petrochemical’s transformation from a “bulk raw material supplier” to a “high-end material solutions provider.” With the continuous development of emerging sectors such as functional membrane materials and biodegradable materials, Hengli Petrochemical is accelerating the establishment of its second growth curve.

Meanwhile, market access qualifications have achieved further breakthroughs. Hengli Fiber and Jiangsu Kanghui have successfully passed the International Automotive Quality Management System certification, obtaining the “passport” to enter the global automotive supply chain, thus laying a solid foundation for expanding into international high-end markets and deepening high-end industrial chain positioning.

III. 2025Year, chemical industry leader"Year of Differentiation"

Placing the annual report of Hengli Petrochemical in the broader context of the 2025 chemical industry can truly reveal its value.

This year, the overall chemical product prices were under pressure: the annual average price of PTA decreased year-on-year, ethylene glycol remained depressed for a long time, and the polyester price spread was squeezed to a historical low. The domestic industry's supply-side competition intensified - with new production capacities being released in a concentrated manner, small and medium-sized enterprises generally fell into a state of loss or minimal profit.

This differentiation essentially reflects the moat formed by “scale + integration + cost control.” The lower the industry’s prosperity, the more pronounced the relative advantages of leading enterprises become.

In terms of innovative R&D, as of the end of 2025, Hengli Petrochemical has cumulatively obtained 2,039 domestic and international patent authorizations, including over 300 newly granted patents in 2025 alone, reflecting its sustained innovation momentum. The collaborative industry–academia–research innovation has achieved remarkable results: the project “Industrialization Key Technologies and Modified Applications of PBS-Type Biodegradable Materials,” jointly undertaken by Kanghui New Materials and Dalian University of Technology, won the Second Prize of the Liaoning Provincial Science and Technology Progress Award, owing to its technological breakthroughs and industrial application value. Underpinning these achievements is Hengli’s quiet yet significant transformation—from “scale-driven” to “technology-driven.”

Four Signals Worth Noting

Signal 1: Non-recurring net profit growth rate (+14.21%)) significantly outpaced the growth rate of attributable net profit (+0.44%))

This discrepancy indicates that in 2024, non-recurring gains (such as investment income and asset disposals) accounted for a significant portion of net profit attributable to shareholders, whereas the core business profitability markedly improved in 2025. This signals an enhancement in earnings quality and warrants investor attention.

Signal Two: Number of Shareholders Decreased by 13.44%Average household market value surged by 51.86%.

Signal Three: R&D expenses decreased by 4.53% year-on-year.

This is a rare warning signal in the annual report. Under the company's narrative of technology-driven transformation, the reduction in R&D investment appears somewhat contradictory. Of course, R&D investment has a lag effect, and the 2,039 patents already authorized in the report indicate that the R&D efforts over the past years have yielded results. However, if this trend continues, it is necessary to be vigilant about the potential erosion of long-term competitiveness.

In 2025, Hengli Petrochemical failed to deliver an impressive growth-oriented financial report. A 15% decline in revenue—on a scale exceeding RMB 200 billion—translates to a loss of over RMB 35 billion in turnover.

However, from another perspective: in a year when the industry is generally under pressure and raw material prices have significantly declined, if a company can achieve "basically stable profits, a significant increase in cash flow, a proactive reduction in financial leverage, and an increase in the profitability of its core business," this is not mediocrity, but rather a way of accumulating strength in a different manner.

Editor: Lily

Data source: Hengli Petrochemical 2025Annual reports, Securities Times, Business Society, Sohu, and other public sources

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

$4 Billion! Medtronic Makes Another Acquisition

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

Profit and Revenue Growth Struggle to Conceal Debt Repayment Pressure; Success of Kingfa Sci & Tech's High-End Strategy Yet to Be Seen

-

Why did a century-old european dental instrument giant relocate its manufacturing hub to china?