Shuffle begins! nine leading plastics companies submit results! esg becomes the new winning track in the industry

In the first week of June, two ESG rating lists coincidentally shone a spotlight on the Chinese chemical industry.

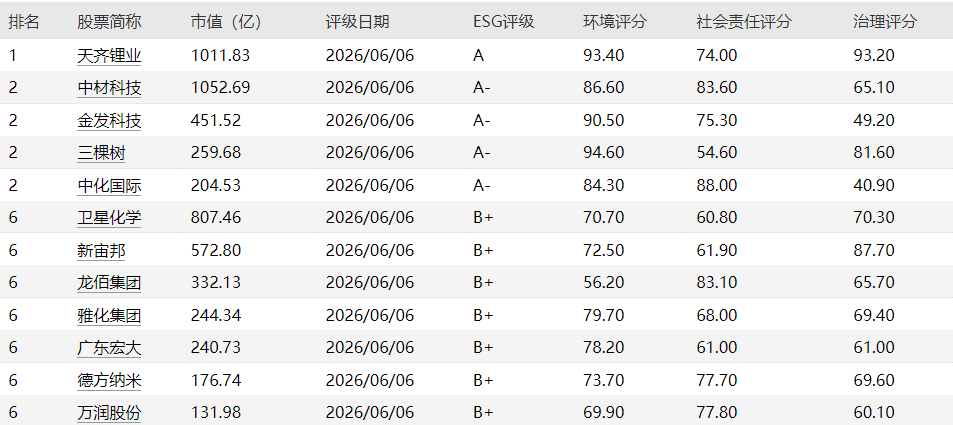

On June 5, Chindings released its latest ESG ratings, in which Guoen Co., Ltd. was awarded an AAA rating—ranking No. 1 among 507 A-share listed companies in the GICS Chemicals industry. Its environmental score reached 99.38, placing it in the top tier alongside industry giants such as Wanhua Chemical and Salt Lake Co., Ltd.

On June 8th, the London Stock Exchange updated its ratings, with China National Materials Technology jumping from C+ to A-. Over four years, it achieved the leap from C to B- to C+ to A-, ranking 2nd among 71 peers. Looking at the list, Jinfeng Technology and Sinochem International also received an A-, placing them in the second tier of the industry.

Figure: Partial screenshot of the London Stock Exchange ESG rating.

Two rating events occurred just three days apart, pointing to the same signal.China’s chemical industry is undergoing a quiet ESG reshuffle.Companies that are among the first to incorporate sustainable development into their annual reports and pour money into green R&D are pulling ahead on rating agencies’ scoreboards.

But ratings are merely superficial. What truly deserves questioning is: how much real money have these companies invested in ESG? How much green DNA is embedded in their new R&D products?

We reviewed the 2025 ESG reports (sustainability reports) of nine representative modified plastics and chemical companies and analyzed them one by one.

1. Kingfa Sci. & Tech.: the “green ambition” of a veteran leader in the modified plastics industry

If there is only one company in the modified plastics industry that can turn ESG into a strategic-level narrative, it must be Kingfa Sci. & Tech.

In 2025, Jinfat Technology delivered an impressive performance report: annual revenue reached 65.396 billion yuan, with a net profit attributable to shareholders of 1.15 billion yuan, representing a year-on-year growth of 39.44%. The sales volume of modified plastic products reached 2.9506 million tons, marking a year-on-year increase of 15.64%, once again setting a global record. The ESG aspect is equally robust.

R&D foundation:In 2025, R&D investment reached RMB 2.76 billion, and the cumulative number of valid invention patents was 2,886. In the chemical new materials industry, these figures are far ahead of the competition.

Carbon emission reduction progress:The carbon emission intensity of domestic modified plastics per unit product (Scope 1 + Scope 2) has been reduced to 0.1305 tons of CO₂ equivalent per ton of product, a decrease of 29.32% compared to 2022—just one step away from the goal of a 30% reduction in carbon emission intensity by 2030.

“The cyclical ambition of "making the utmost use of resources."Green plastic output reached 309,400 tons, waste plastic recycling volume reached 272,000 tons, and recycled plastic output reached 379,000 tons. The 2030 targets for all three categories are 1 million tons.

Image source: Kingfa Sci. & Tech.

Accelerating Clean Energy:Self-generated and self-consumed photovoltaic power reached 83.34 million kWh, surging 250% year-on-year; green electricity purchases totaled 70.15 million kWh.

The product side is also clear: 50,000 tons/year of bio-based succinic acid and 10,000 tons/year of bio-based BDO are steadily being produced, with sales of biodegradable plastics reaching 226,300 tons. The combination of "bio-based materials + recycling + low-carbon modification" is reshaping the green value chain of modified plastics.

2. Guoen Co., Ltd.: The Hidden Expert That Achieved a "Full Score" with Its First ESG Report

In terms of scale, Guoen Co., Ltd. recorded revenue of RMB 21.251 billion and net profit attributable to shareholders of RMB 841 million in 2025, ranking second only to Kingfa Sci. & Tech. in the modified plastics industry. In terms of ESG, its story is even more striking — 2025 marked the first year that Guoen Co., Ltd. released a sustainability report, and this ESG report immediately earned a AAA rating from Zhidings, with an environmental score of 99.38, ranking No. 1 in the industry.

Guoen Corporation also has a solid R&D foundation: in 2025, it invested RMB 694 million in R&D, accounting for 3.27% of its revenue, employed 761 R&D personnel, accumulated 521 patents, participated in the formulation of 16 national standards, 19 group standards, and 4 industry standards, and owns 10 high-tech enterprises under its umbrella.

On the green products front, Guoen Holdings’ PCR (post-consumer recycled) plastics system is a highlight:Covering multiple categories including HIPS, ABS, PC/ABS, and PP.The recycled material content in some products can reach over 90%.It has been applied in batches in the fields of home appliances, displays, and electronic products. In 2025, the company was recognized as a provincial-level green factory and a provincial-level manufacturing single champion.

However, this first report also exposes typical novice issues: Scope 3 emissions have not yet been disclosed, and the quantitative management of carbon emissions is still at an early stage.

In February 2026, Guoen Co., Ltd. completed its H-share listing, establishing an “A+A+H” three-market capital presence. The depth and breadth of its ESG information disclosure will face more stringent scrutiny from the Hong Kong stock market.

III. Dawn Polymer: Distinctive Strength in Elastomers, but Pronounced Imbalances in ESG Performance

Daon Co., Ltd. is a unique presence in the modified plastics industry—it does not pursue scale dominance, but instead focuses on thermoplastic elastomers and adopts a differentiated approach.In 2025, the company’s revenue exceeded RMB 6 billion for the first time, reaching RMB 6.056 billion. Net profit attributable to shareholders of the parent company was RMB 189 million, up 34.03% year on year, and product sales surpassed 556,100 tons, all hitting record highs.

On the R&D front, Dawn Co., Ltd. invested RMB 280 million (accounting for 4.62% of revenue), established a “1+2+4+10” R&D system, and owns seven high-tech enterprises.The most notable technological breakthrough is the use of highly gas-barrier layer materials in DVA tires.Only ExxonMobil and Dow possess the relevant production technology worldwide. This achievement was selected as one of Shandong Province’s Top Ten Scientific and Technological Innovation Achievements of 2025, and is expected to be launched on a large scale in the second half of 2026. The company has also expanded into cutting-edge materials such as elastomers for robotic bionic skin.

In green collaboration, Dawn established Qingdao Haier Environmental Materials Technology Co., Ltd. as a joint venture with Haier, entering the circular economy sector, and participated in bio-based materials projects with Sony and Samsung. Environmental protection investment totaled RMB 32.31 million, and the waste recycling and reuse rate reached 93%.

IV. Qide New Materials: A “Small Player” with an AA ESG Rating

Among the nine companies, Qide New Material (300995) is the one that is most easily overlooked—its revenue in 2025 is only 375 million yuan, with a net profit of 19.63 million yuan, a scale that is less than 1/170 of Jinhua Technology. However, its performance in ESG has made many large enterprises feel ashamed.

Qides New Materials’ ESG foundation stems from its business model: focusing on functional polymer composite materials, carbon fiber products, and precision molds. The logic of “replacing steel with plastic and wood with plastic” is inherently a green substitution strategy. In 2025, overseas revenue reached RMB 64.86 million, surging 96.27% year on year, while revenue from the Thailand plant grew 332.57% year on year. The rapid growth of its overseas business has created a mandatory requirement for ESG disclosure.

On the green products front, the company has developed high-temperature-resistant nano polyamide engineering plastics, low-odor and low-VOC modified plastics for automotive interiors, and intelligent low-dielectric materials, all targeting strategic emerging sectors such as new energy vehicles and aerospace. Its carbon fiber products have been designated for multiple vehicle models and have also secured orders for humanoid robots.

The company also plans to achieve breakthroughs in 10 bottleneck technologies and will continue to increase investment and expand production at its Thailand factory and in its carbon fiber products business. For a company with annual revenue of less than RMB 400 million, the very fact that it dares to talk about “Scope 3” in its ESG report and set goals for tackling critical choke-point technologies is, in itself, an attitude.

5. Huitong Corporation: Turning PCR into a “Moat”

Huitong Co., Ltd. has chosen a more focused ESG path: to persistently pursue a circular economy, turning post-consumer recycled materials (PCR) from a concept into an industrial chain.

In 2025, Weitong Co., Ltd. achieved a revenue of 6.49 billion yuan, with R&D investment of 306 million yuan (accounting for 4.71% of revenue). The proportion of R&D personnel reached 26.43%, with a total of 314 authorized patents and participation in the formulation and revision of 28 national standards.

Image source: Huitong Co., Ltd.

In the PCR sector, Huitong Co.’s can be described as aggressive: it established a wholly owned subsidiary, “Huitong Environmental Protection,” to build a closed loop of “collection — recycling — high-value-added application”; its joint-venture base, Guangdong Zhongyin Plastic, has an annual capacity of 100,000 tons, and Huifeng Environmental Technology has an annual capacity of 50,000 tons. Its recycled materials have obtained 182 international certifications, including GRS and UL2809, covering the full range of PE, PP, ABS and other product categories, and PCR materials reduce carbon emissions by more than 200,000 tons annually.

On the clean energy front, the share of green electricity increased to 11.40%, and the rooftop photovoltaic system at the Anqing plant generated 6.17 million kWh of electricity annually. The company is targeting its long-term goal of achieving carbon neutrality across its own operations and value chain before 2050.

The challenge is equally clear: Scope 3 emissions account for 91.7% of total emissions, and supply chain emission reduction targets have yet to be set. The tension between business expansion and decarbonization goals is a common growing pain in the modified plastics industry.

VI. Wote Co., Ltd.: Developing Green Materials from the Source Through Synthetic Biology

Wote Co., Ltd. has moved beyond the traditional scope of “modified plastics” and is positioned as a specialty polymer materials platform.

In 2025, the company's revenue reached 2.052 billion yuan, with a net profit attributable to shareholders of 64.3972 million yuan, a year-on-year surge of 75.97%. Revenue from specialty polymer materials was 1.013 billion yuan, accounting for 49.37% of total revenue, nearly half of the total.

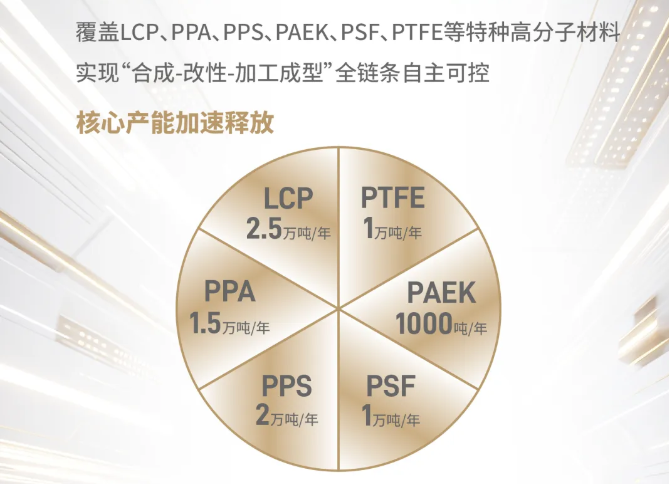

LCP(Liquid Crystal Polymer):The Chongqing base with an annual production capacity of 25,000 tons of synthetic resin will be put into operation in May 2025, making Watte the largest LCP supplier in the world. LCP is a core material for high-frequency communications in 5G/6G and AI high-speed connectors.

PEEK(Polyether ether ketone)The pilot production of the first-phase production line has begun, and Zhejiang Kesai possesses the processing capability for hundred-ton PEEK profiles—an essential lightweight material for humanoid robots and the low-altitude economy.

Bio-based matrix:Bio-based high-temperature nylon, transparent nylon, long-chain nylon, and nylon elastomers have all entered mass production. In collaboration with the Shenzhen Institutes of Advanced Technology, Chinese Academy of Sciences, we have jointly established the “Joint Innovation Center for Synthetic Biochemistry Applications” to develop green materials from the source of synthetic biology.

Source: Water Co., Ltd.

Cyclical innovation:Automotive OEMs have applied low-carbon PCR materials at scale and innovatively used recycled carbon fiber to manufacture robot skeletons and robotic arms. In 2025, R&D investment reached RMB 123 million, accounting for 6% of revenue, with a cumulative total of 434 patents.

7. China Resources Materials: Telling the Story of the Circular Economy with 477 Million Plastic Bottles

China Resources Materials is the listed new chemical materials platform under China Resources Group, primarily engaged in polyester (PET) materials. In 2025, its Wind ESG rating rose from A to AA, ranking fourth in the basic chemicals industry, and it was selected for the “ESG Golden Bull Award Top 100.”

Although affected by industry cycles in 2025, the company recorded revenue of RMB 13.068 billion (down 27.62% year on year) and a net loss of RMB 86 million (narrowed by 84.88% year on year), yet it did not slow down on the ESG front. R&D investment amounted to RMB 24.4188 million, with 148 R&D personnel and 74 valid patents in total. PETG products expanded into emerging fields such as 3D printing, with sales volume increasing by 270% year on year.

China Resources Materials’ most prominent ESG story is circular economy.

rPETIndustrialization of the chemical bottle-to-bottle recycling technology.Sales volume of 25% rPET food-grade recycled polyester surged from 16,000 tons to 34,000 tons (a year-on-year increase of 113%). Over the year, approximately 8,600 tons of recycled waste PET bottle flakes were used, equivalent to the recycling and reuse of about477 million discarded plastic bottlesreducing carbon emissions by approximately 25,000 tons. The company also took the lead in formulating the group standard for Recycled Polyethylene Terephthalate (rPET) Resin for Bottles.

In terms of carbon reduction, the comprehensive energy consumption per 10,000 yuan of output value decreased by 10% compared with 2020 (achievement rate: 106.19%), and CO₂ emissions per 10,000 yuan of output value decreased by 5% compared with 2020 (achievement rate: 126.3%), both exceeding the targets. The cumulative net power generation of the photovoltaic project at the Changzhou base reached 11.5216 million kWh. The comprehensive utilization rate of waste increased from 91.03% to 95.88%, and SO₂ emissions decreased by 39.08% year on year.

As a subsidiary of a central enterprise, China Resources Materials has its ESG genes deeply embedded in its governance structure—its board of directors has established a Strategy and Sustainable Development Committee, and ESG performance has been incorporated into the assessment of senior executives.

VIII. Sinochem International: An “ESG Model” for the Transformation of Central State-Owned Enterprises

As a representative of central state-owned enterprises, Sinochem International’s ESG narrative is particularly substantial—this is the company’s 22nd sustainability report. It has received an AA rating from Wind ESG and an A- rating from the London Stock Exchange, with a social responsibility score of 88.00, ranking first in the chemicals industry.

In 2025, the company recorded revenue of RMB 47.34 billion. Although it posted a net loss of RMB 2.223 billion, marking its third consecutive year of losses, its ESG investment did not shrink: total environmental protection investment reached RMB 446 million, R&D investment stood at RMB 687 million, and revenue from new product sales amounted to RMB 7.47 billion, representing a production value ratio of 15.78%.

In terms of carbon reduction, CO₂ emissions per 10,000 yuan of output value decreased by 24% compared with 2020, and comprehensive energy consumption per 10,000 yuan of output value decreased by 15%, both meeting the “14th Five-Year Plan” targets. The share of renewable energy increased from 0.3% in 2024 to 6.5%. Waste recycling and reuse reached 216,400 tons (up 34.8% year over year), and the water reuse rate reached 98%.

Product side: A 2,500-ton/year para-aramid capacity expansion project was completed and put into operation, and MIAK specialty ketone was industrialized and brought online. Fourteen enterprises completed ERP upgrades; Sinochem High Fiber passed the MIIT AAALevel 4 Assessment for Integration of Informatization and Industrialization (among the first batch nationwide), and Sinochem Yangzhou Lithium Battery established an AI-enabled flexible intelligent factory.

Sinochem International successfully issued its first phase of sustainable development-linked medium-term notes (totaling 1.5 billion yuan), with financing costs directly linked to energy-saving and emission reduction targets.

IX. Wanhua Chemical: The “Green Addition and Subtraction” of a Chemical Industry Giant

Putting Wanhua Chemical in this review seems a bit like "dimensionality reduction" — revenue in 2025.203.235 billion yuan, net profit attributable to the parent company was 12.527 billion yuan, total assets were 323 billion yuan, and R&D investment alone reached as high as4.865 billion yuan(accounting for 2.39% of revenue), with more than 1,230 invention patents filed throughout the year. It is a global leader in polyurethanes and the flagship of China’s chemical new materials industry.

Precisely for this reason, Wanhua Chemical’s ESG performance is all the more meaningful as a benchmark—showing just how high the industry’s ceiling can be.

This is Wanhua Chemical’s third ESG report. It was prepared with reference to the Shanghai Stock Exchange guidelines, the GRI Standards, and the TCFD framework, incorporates a double materiality analysis, and has been assured under limited assurance by SGS. In the Zhiding rating system, Wanhua is rated AAA, tied with Guoen Co., Ltd. The report identifies four double materiality topics: occupational health and safety, climate change response, energy use, and chemical safety.

Carbon reduction target:By no later than 2030, the carbon peak will be achieved, aiming for carbon neutrality by 2048. The total carbon emissions for Scope 1 and 2 will reach 31.32 million tons of CO₂e by 2025 (an increase of 11.7% year-on-year due to new projects coming online), while the share of clean electricity will rise from 13.97% to 30.83%—through collaborations such as Haiyang Nuclear Power and Fuqing Nuclear Power, with an annual electricity trading volume of 3.97 billion kilowatt-hours.

Green Product Matrix:Low-carbon lithium battery material Wanlium CS adopts continuous graphitization technology, significantly reducing energy consumption compared with traditional processes; MDI-molded pallets have a carbon footprint of only 5.967 kgCO₂e, reducing carbon emissions by 50%–70% compared with traditional pallets; bio-based paper cup coatings increase the recyclability of paper cups from 40% to 85%.

Circular Economy:Waneco rPC recycled polycarbonate reduces carbon emissions by over 80%; fully biodegradable film tested in 23 rice production areas nationwide; solid waste landfill rate is only 0.3%, having achieved the 2030 target of ≤0.5% ahead of schedule; cooling water recycling rate is 99.0%.

Wanhua Chemical’s ESG governance is also noteworthy: the Board of Directors has established a Strategy and Sustainability Committee, ESG performance has been incorporated into the comprehensive performance evaluation of senior management, and 100% of newly added suppliers are covered by sustainability audits.

But this “giant elephant turning around” also comes with growing pains: due to the intensive commissioning of new projects, total carbon emissions and energy intensity have shown a short-term upward trend, with energy consumption per unit of product rising from 122 in 2023 to 138 kilograms of standard coal per ton in 2025.The tension between scale expansion and carbon reduction is the most critical ESG issue for Wanhua Chemical in the next decade.

Summary: Commonalities and Differences Among the Nine Companies

Looking at these nine reports together, the commonalities are clear, and the differences are equally pronounced.

Commonality One: R&D is ESG.Wanhua Chemical 4.865 billion, Jinhfa Technology 2.76 billion, Guoen Co., Ltd. 694 million, Sinochem International 687 million, Huitong Co., Ltd. 306 million, Daon Co., Ltd. 280 million, Water Co., Ltd. 116 million—R&D investment is the foundation of green products. In the chemical new materials industry, "green" is not just a label, but a full-chain engineering capability from molecular design, raw material selection, process routes to recycling solutions.

Commonality Two: The circular economy has shifted from being an "optional extra" to a "mandatory question."The driving force behind Kingfa’s “making full use of plastics,” China Resources Materials’ rPET recycling of 477 million plastic bottles, Huitong’s 182 internationally certified products, Guoen’s use of 90% recycled PCR content, and Wanhua Chemical’s rPC and biodegradable mulch film is simple: downstream automakers, home-appliance manufacturers, consumer electronics companies, and beverage brands are writing recycled-content requirements into their procurement standards.

Commonality 3: Carbon emissions reduction is beginning to be tied to tangible financial incentives.Sinochem International's 1.5 billion sustainable bonds, Wanhua Chemical's 39.7 billion kWh nuclear green electricity transactions, and Jinfa Technology's self-use photovoltaic soaring by 250%—ESG is transforming from a cost center into a competitive factor.

Commonality Four: Ratings are widening the gap.Wanhua Chemical and Guoen Co., Ltd. secured Zhidin AAA ratings; Kingfa Sci. & Tech., Sinochem International, and CR Materials remained firmly in the A- to AA range; Qide New Materials obtained a Huazheng AA rating with revenue of less than RMB 400 million; while Dawn Polymer’s carbon emissions data still contains large gaps.

But the divergence is equally stark: within the same industry, companies are already starting from different ESG baselines.Companies with high ESG ratings are using green financing to lower their cost of capital and leveraging certified credentials to expand into overseas markets; those with low ratings, by contrast, may gradually fall behind in supplier screening by downstream customers. Wanhua Chemical’s case also reveals a deeper tension: how to balance business growth with control over total carbon emissions—a challenge that no chemical company can avoid as it scales from the tens of billions to the hundreds of billions.

The ESG arms race in China’s chemical industry has already begun.The weapons of competition are not public relations rhetoric, but rather biological production capacity, the number of PCR certifications, green electricity contracts for nuclear power plants, and patent certificates in laboratories.

From Qide New Materials with revenue of RMB 375 million to Wanhua Chemical with revenue of RMB 203.2 billion, from a first ESG report to a 22nd sustainability report — the ESG narrative in China’s chemical industry is evolving from “whether it exists” to “how good it is.” In this round, some companies have already written chapters rich in data and detail, while others are still lingering in the preface.

Editor: Lily

Sources: Baijiahao, Eastmoney Research Reports, ZhiDing ESG Rating Database, Wind ESG Rating Database, Sino-Securities ESG Rating Database, Shenzhen Stock Exchange Listed Company Information Disclosure Platform, Shanghai Stock Exchange Listed Company Information Disclosure Platform, and ESG reports officially released by each company.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Government's Triple Action, Enterprises' Three Arrows in Five Days, Semiconductor Reshuffle! What Signal Does Japan's Chemical Industry Release?

-

Name change without tax change: POM Anti-Dumping Duty Rate Inheritance Implemented

-

Fire breaks out at jiangsu meiside!

-

Ethylene: Production Capacity Accelerates Expansion, Global Industry Landscape Is Being Reshaped