Shutdowns And Production Cuts! Widespread Price Quotes Suspended, Chemical Products May Still Be Easier To Rise Than Fall In June-July!

Recently, the three global chemical giants BASF, Huntsman, and Covestro issued MDI price increase notices in concentrated fashion at the end of May: BASF raised prices by $0.35 per pound (approximately RMB 5,260 per ton) starting May 29; Huntsman raised prices by $0.24 per pound (approximately RMB 3,610 per ton) starting May 22; and Covestro raised prices by $0.22 per pound (approximately RMB 3,310 per ton) starting July 1. The synchronized moves by the three giants are a clear signal that the market is expected to continue trending upward in the second half of the year.

Japanese Kansai Paint has issued a price adjustment notice: effective June 15, solvent-based coatings will be increased by 20%–35%, water-based coatings by 15%–30%, and powder coatings by 15%–25%.

The price increase of Kansai Paint is not an isolated case; it reflects a rare large-scale supply contraction currently occurring in the global chemical industry. Since 2026, there has been a complete shutdown of world-class facilities in Jubail, Saudi Arabia, a historic capacity reduction in the petrochemical industries of Japan and South Korea, a dual supply shock in the North American MDI market, and an accelerated exit of high-cost capacity in Europe, leading to a continuous widening of the supply-demand gap.

Industry insiders generally believe that, driven by multiple factors, the prices of chemical raw materials are likely to continue an upward trend in the future, placing ongoing cost pressure on downstream industries such as plastics, coatings, fertilizers, automobiles, and household appliances.

The global industrial production cuts and shutdowns in the first half of 2026 present four distinct core focal points.

Middle East: Eye of the Geopolitical Storm - Supply Chain Disruption

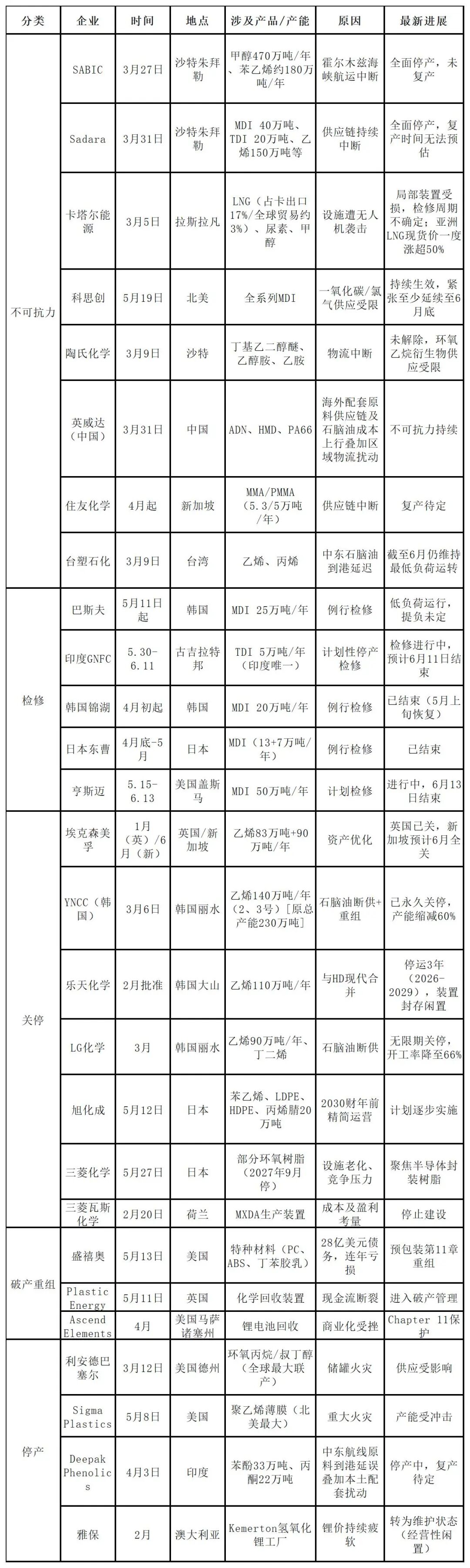

Saudi SABIC has announced force majeure on its styrene monomer and methanol production. Its methanol plant in Jubail has an annual capacity of 4.7 million tons, making it the world’s largest single-site methanol production facility. Meanwhile, Sadara’s 400,000-ton MDI and 200,000-ton TDI units have been completely shut down, causing over 90% of MDI/TDI supply in the Middle East to disappear instantly. QatarEnergy’s LNG facility has also been partially damaged, accounting for about 17% of Qatar’s exports, with a highly uncertain maintenance period. As of now, these facilities have not resumed operations, and their restart is highly dependent on the easing of geopolitical tensions.

Asia (Japan and South Korea): Passive Transformation Under Supply Disruption - Japan's Ethylene Operating Rate Falls to Historic Low

The petrochemical industries of Japan and South Korea are heavily dependent on naphtha from the Middle East (about 80% of Japan’s and over 70% of South Korea’s imports must pass through the Strait of Hormuz). After the supply cutoff, Japan was hit particularly hard: in April, ethylene operating rates fell to 67.3%, the lowest level since 1996, leaving nearly one-third of capacity idle; ethylene output plunged 37.1% year on year. Downstream derivatives fell in tandem—March production of high-density polyethylene dropped 61.6% year on year, low-density polyethylene fell 40.6%, polypropylene declined 28.3%, and PVC contracted for six consecutive months.

Japanese companies are accelerating the divestment of traditional petrochemical businesses. Asahi Kasei has announced a significant reduction in domestic petrochemical derivative production capacity by May 2026, aiming to gradually exit domestic production of styrene monomers and polyethylene by the fiscal year 2030. Mitsubishi Chemical and Mitsui Chemicals are also advancing similar divestments.

In South Korea, the petrochemical industry is deeply involved in integrated capacity reduction: YNCC has permanently closed two cracking units (1.4 million tons/year, reducing capacity by 60%); Lotte Daesan has temporarily shut down its 1.1 million tons of ethylene for three years; LG Chem's Yeosu plant has indefinitely shut down its 900,000 tons of ethylene. The top ten petrochemical companies in South Korea plan to collectively reduce cracking capacity by about 25% between 2026 and 2028.

North America: MDI Supply Crisis and Bankruptcy Wave Concurrent

The North American MDI market is facing a rare double blow: Covestro has declared force majeure due to restricted supplies of carbon monoxide and chlorine, with the tight situation expected to last at least until the end of June; Huntsman’s Gexma 500,000-ton MDI facility is undergoing maintenance until June 13, resulting in a combined capacity restriction of about 800,000 tons. Meanwhile, Shengxiao has entered bankruptcy restructuring due to $2.8 billion in debt and three consecutive years of losses, becoming a landmark case in the current financial crisis of specialty materials companies.

Europe: High-Cost Assets Accelerate Their Exit

Europe has seen the longest-lasting wave of shutdowns. ExxonMobil’s early closure of its 830 ktpa ethylene unit in Fife, UK, signals that Europe’s aging ethylene capacity no longer has room to survive in global competition; its 900 ktpa ethylene unit in Singapore is also scheduled for a full shutdown in June. SABIC and LyondellBasell have respectively sold their European olefins/polyolefins assets to AEQUITA, BASF has launched the largest “core transformation” program in its history—targeting a 20% reduction in fixed costs for its core businesses by 2029—and Solvay is gradually shutting down part of its inorganic operations in Germany. Europe is shifting from basic chemicals toward higher-value specialty chemicals, but in the short term, ongoing capacity rationalization will continue to drive up the region’s dependence on imports.

Global Production Halts/Maintenance/Force Majeure Panorama

The table below systematically summarizes the major production suspensions, force majeure events, maintenance shutdowns, and closures in the global chemical industry in the first half of 2026.

Large-scale suspension of reports! Rigid contraction on the supply side is accelerating its transmission.

The shockwaves from the global wave of production shutdowns have reached China’s domestic chemical market. On June 2, widespread suspensions of quotations occurred across the domestic chemical market. According to incomplete statistics, on June 2, about 230 domestic companies (including 198 producers and 32 trading companies) were involved, covering more than 30 major categories of chemical products. The number of suspended quotation entries in a single day increased by about 120% compared with the daily average in May, marking the widest and largest-scale quotation stagnation in the market over the past month.

An in-depth analysis of the reasons for suspension shows that 89 entries, accounting for 32.25% of the total, were due to no goods available or quotations being suspended because the plant was shut down, out of operation, or under maintenance, making this the primary underlying cause. Among the remaining entries, 27.54% stopped external sales because of “self-use by the company / orders fully booked,” while 18.48% were due to “low inventory / one-off negotiation.” Another 21.73% did not specify a clear reason. This round of quotation suspensions was highly concentrated in Shandong Province, with 116 entries in total, accounting for 42.03%. Dongying, Weifang, Zibo, Binzhou, and other petrochemical and chemical industry clusters were the main concentration areas. East China (Jiangsu, Zhejiang, and Anhui) accounted for 21.01%, while Central China (Hubei and Henan) accounted for 15.22%.

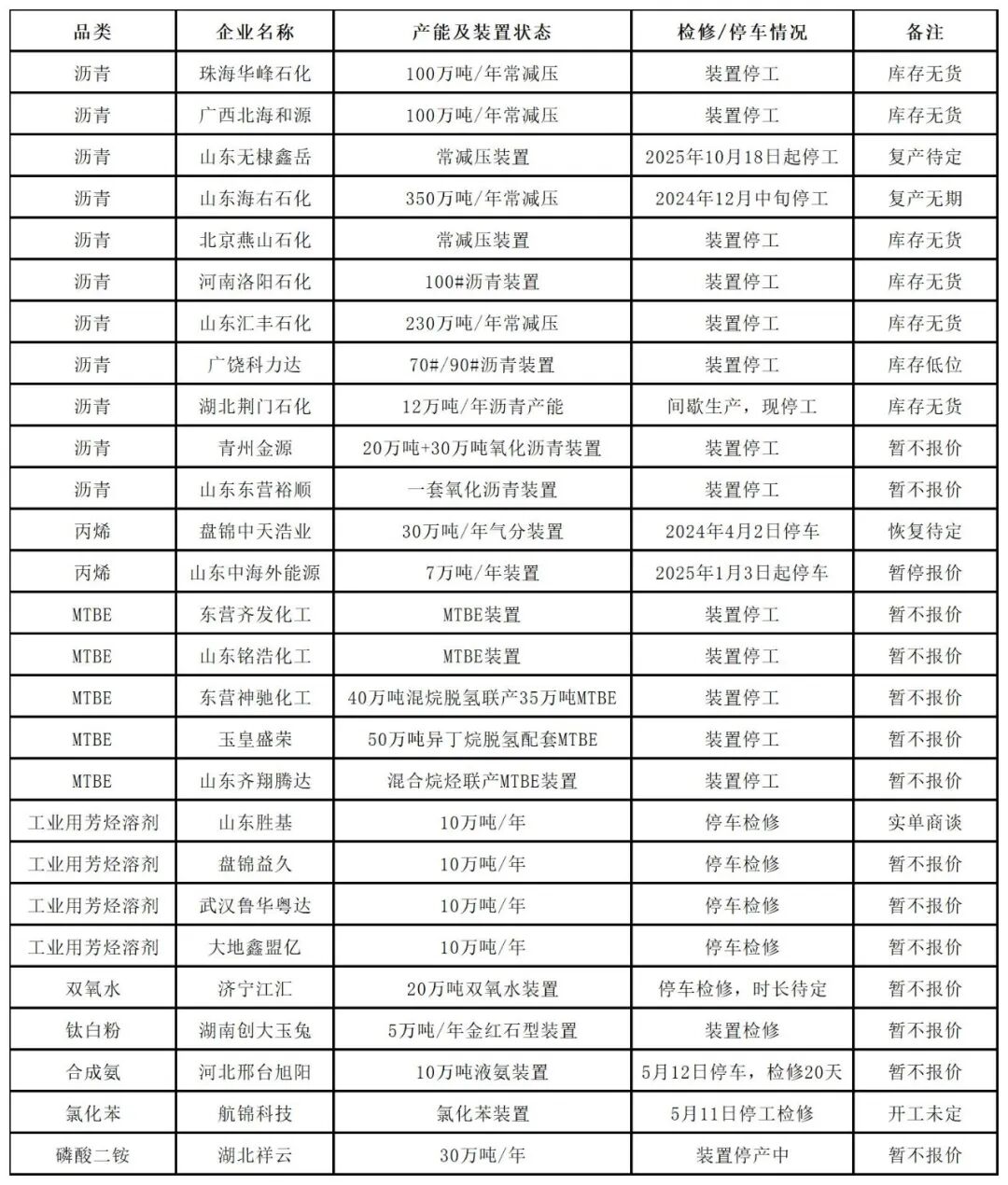

Summary Table of Shutdown/Maintenance Status of Key Units (June 2)

As can be seen from the table, the supply contraction trend spans multiple sectors, ranging from energy fuels to basic chemicals, fertilizers, and new materials. In the asphalt industry, 11 refineries stopped quoting due to unit shutdowns, and the asphalt operating rate fell to 15.0%, down 13.8 percentage points year-on-year, hitting a new low in recent years. In the MTBE industry, five key units were shut down, and the market operating rate dropped to 47.68%, down 6.36 percentage points month-on-month. The propylene market has remained out of stock due to long-term shutdowns of units.

In addition, companies have shifted from relying solely on passive shutdowns for maintenance to a parallel strategy of passive shutdown maintenance and proactive supply management. In addition to complete shutdowns, many companies have reduced spot supply by cutting production or prioritizing internal use. The diammonium phosphate units of Anhui Liuguo Chemical and Hubei Yidu Xingfa are “operating at reduced rates”; Luxi Chemical’s chloromethane unit is “running at low load.” Intermediate products such as synthetic ammonia and methanol have seen widespread suspension of quotations as companies prioritize internal use—many synthetic ammonia producers, including Henan Jindadi, Shanxi Fengxi, Shaanxi Shanhua, and Hubei Yangfeng, as well as Zhejiang Satellite Chemical (whose propylene is mainly for internal use, with no supply for external sales), have stopped quoting because their products are not sold externally, indicating a deepening level of integration and supporting capacity within industrial chains.

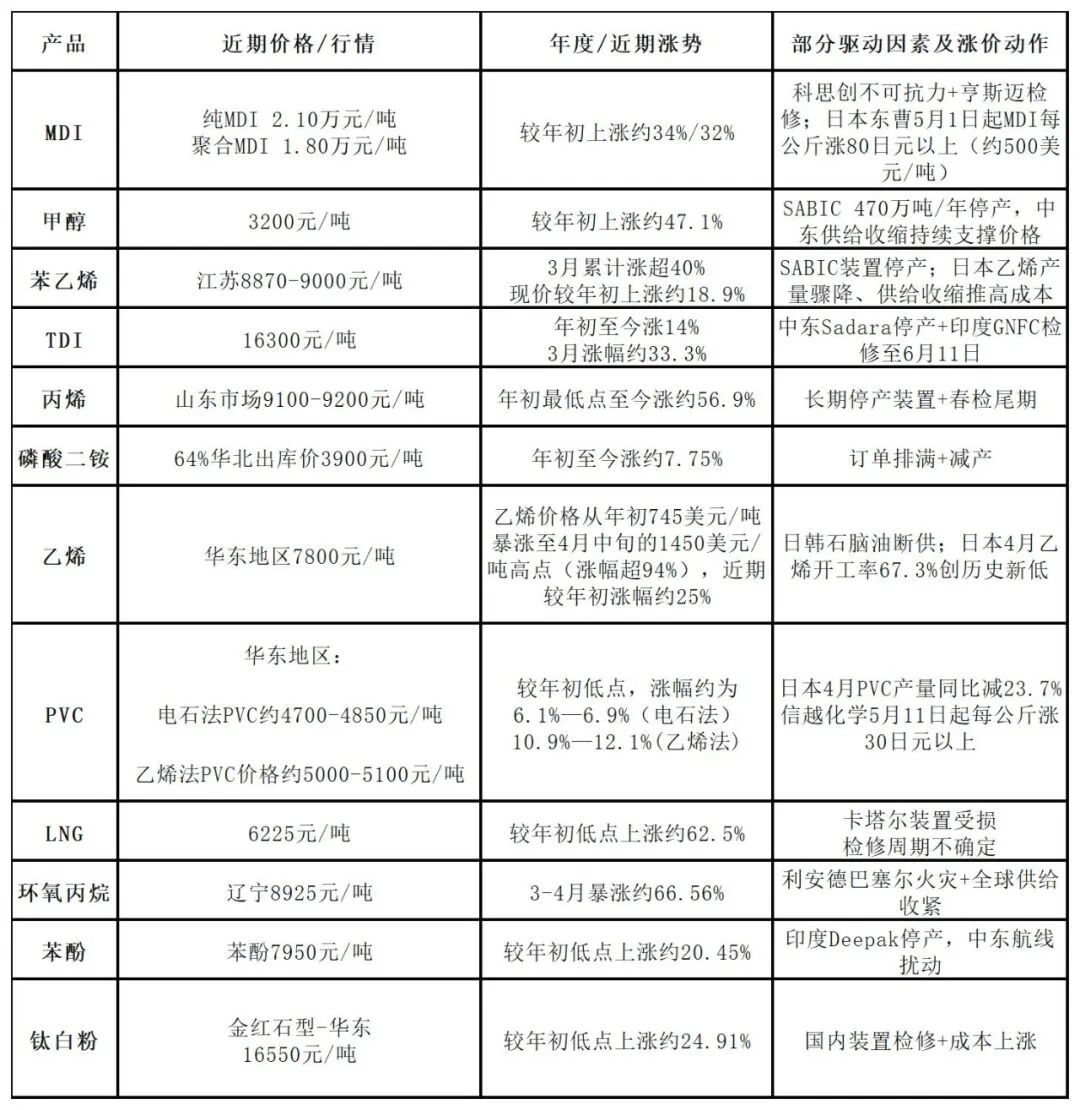

The continued contraction in the supply side has been fully reflected in prices. As of June 2, 2026, some of the latest prices remain at elevated levels. Although some products have seen temporary pullbacks due to weak short-term demand, over a longer time frame, the annual gains of most chemical products are still staggering. In particular, entering May, global plastics and chemicals giants sent out price increase notices in quick succession. Companies such as BASF, Dow, Celanese, Mitsubishi, and Tosoh covered multiple core categories including PE, PA, ABS, POM, and MDI, with a maximum single increase of as much as RMB 6,100 per ton.

Below are the latest prices, price increase trends, and implementation status of price increase notices for the major affected products:

Although the recovery in downstream demand remains uncertain, the supply-side contraction is more certain: the restart of Middle Eastern facilities remains indefinitely delayed, MDI tightness in North America is expected to last at least until the end of June, ethylene operating rates in Japan are still far below normal levels, and in China, the tail end of spring maintenance combined with weak profitability means that supply will be difficult to ease in the short term.

Industry insiders believe that, with the summer gasoline peak season, the peak demand season for downstream coatings and plastic products, and the continued escalation of the U.S.-Iran standoff all converging, June and July will remain a critical window during which chemical product prices are more likely to rise than fall.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Government's Triple Action, Enterprises' Three Arrows in Five Days, Semiconductor Reshuffle! What Signal Does Japan's Chemical Industry Release?

-

Name change without tax change: POM Anti-Dumping Duty Rate Inheritance Implemented

-

Fire breaks out at jiangsu meiside!

-

Ethylene: Production Capacity Accelerates Expansion, Global Industry Landscape Is Being Reshaped