Internal and external challenges intertwined! even the "survivors" after an unprecedented production halt in the textile industry may not become kings

In recent years, the competition within the textile industry has intensified, and this year it has faced unprecedented internal and external challenges. It is clear to anyone with insight that limitless competition will only harm the industry, and even the last ones standing may not necessarily emerge as the winners.

Unprecedented wave of production shutdowns

This summer, the textile industry experienced an unprecedented wave of production stoppages.

In recent years, regions with rapid capacity growth, such as Xinjiang, northern Jiangsu, and Henan, have already seen significant shutdowns. These shutdowns also include some machines that were recently put into operation in the past two years, which have higher profitability than older machines and face substantial cost recovery pressure. They will only choose to shut down as a last resort.

Some traditional textile clusters in the Yangtze River Delta region are relatively better off, with smaller scales of production stoppages. These companies have been operating for many years, so their customer base and product sales channels are relatively more stable. They also have a certain level of technological accumulation, allowing them to produce higher-end products, but there are still some measures in place to reduce production.

According to normal market trends, this wave of production halts is expected to last for at least another month.

Unprecedented external challenges

In addition, the black swan events that have occurred from time to time over the years, along with the increasingly advanced textile industry overseas, have brought unprecedented challenges to domestic textile enterprises.

In terms of tariffs, the indiscriminate taxation imposed by the United States on the entire world is something that most people did not anticipate. As one of the most important textile consumption markets globally, the U.S. has universally increased tariffs on all textile-exporting countries. This not only has a significant impact on clients in the U.S., but also affects businesses engaged in domestic trade and those in other countries whose impact was originally minimal. When the U.S. reduces its orders, the companies that previously relied on U.S. orders will compete in other markets, driving prices lower and lower.

In terms of shipping, the Red Sea crisis has not only increased freight costs due to the need to detour around the Cape of Good Hope, but it has also lengthened the shipping time, resulting in delays in the recipient receiving their goods. This, in turn, has effectively extended the payment terms and compressed cash flow.

In terms of homomorphic competition, the textile industry in Southeast Asia and Central Asian countries has experienced rapid development in recent years and is naturally not satisfied with merely being an OEM. They are beginning to extend upstream and downstream in the industrial chain. If it comes to direct competition, Chinese enterprises are certainly not afraid, but they will also want to protect their domestic industries. This year, India has implemented restrictions on the import of Chinese textile machinery.

The survivor is not necessarily the king.

There is a saying in the market: "The remaining ones are kings." It means that in the end of competition, the surviving enterprises can capture most of the market and become the winners. In the past few decades, there have been many examples of textile companies that turned around with just a few orders when they were in dire straits, so many textile companies hold on to this idea as well.

Many textile enterprises are holding on, thinking that if they endure this period, everything will get better. But times have changed; in the current situation, merely surviving does not guarantee success. Currently, in the textile market, the production capacity of conventional products is the least valuable, and it is very difficult to eliminate this capacity. This surplus situation is expected to continue for a long time.

Under the conditions of excess capacity, even if the market really shows signs of recovery, unless there are some companies that have already established a competitive advantage in certain aspects, it will be very difficult for most textile enterprises to earn excess profits.

The urgency to combat involution is imminent.

In March of this year, the government work report explicitly emphasized the need to adjust the competition characterized by "involution"; on June 27, the new "Anti-Unfair Competition Law" was revised and will come into effect on October 15 of this year; on July 1, the Central Financial Committee meeting again proposed "anti-involution" competition, addressing the issue of chaotic low-price competition among enterprises and promoting the orderly exit of backward production capacity.

On the same day, the magazine "Qiushi" published an article titled "Deeply Understand and Comprehensively Rectify 'Involutionary' Competition." The article states that "involutionary" competition confines various entities to a low-price, low-quality, and ineffective competition, breaking through the boundaries and bottom lines of market competition, disrupting market order, and allowing its development will lead to endless harm.

In the case where the market's self-regulation fails, it is hoped that administrative measures can bring the textile industry back to a healthy development track.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

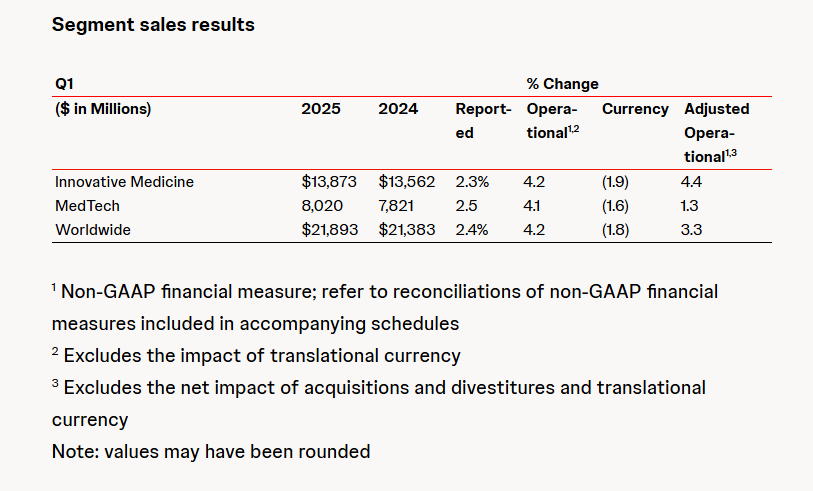

Abbott and Johnson & Johnson: Global Medical Device Giants' Robust Performance and Strategies Amid Tariff Pressures

-

BYD releases 2024 ESG report: Paid taxes of 51 billion yuan, higher than its net profit for the year.

-

The price difference between recycled and virgin PET has led brands to be cautious in their procurement, even settling for the minimum requirements.

-

Which brand of AI TV is good? Samsung Vision AI interprets the new industry standard with its "technical advantage."

-

Why is milk not packaged in aluminum cans?